Startups to Watch

Happy Wednesday!

Aaaaand we are back! For those who are new, this series is dedicated to early stage startups that are under the radar – and have a good story to tell. I send it out every other Wednesday (sometimes every week)- and it is separate from my traditional weekly newsletter. The basic criteria is a company that is not on the spotlight and is NOT actively raising proceeds. There is also no bias – apart from the fact that I like the story. I am not an investor or get any financial compensation to promote startups featured. This is intended for informational purposes only, using my solid base of subscribers to share intel of good people doing cool things.

Since launch, featured startups in aggregate were connected 64 times, to 32 different investors/strategic partners globally.

Finally, if you are a founder and want to be considered for this series - it is very simple:

Please fill out a one-pager, in English, about your company using the topics and themes outlined in the posts.

Reply to this e-mail with your one-pager attached.

I will review and reach out if I need more information.

It will be posted if I believe the startup fills the profile and audience of this newsletter.

Good Luck!!!!!!

Follow me on LinkedIn , Instagram or Twitter for daily updates!

Opinions expressed here are solely my own and does not represent those of people, institutions, organizations that I may or may not be associated with in any capacity, unless explicitly stated.

Enormous Opportunity:

Card networks have built massive, lucrative, and resilient revenue streams: their interchange fees totaled over $50 billion globally (excluding financial revenues) in 2020, at a time when extending payment terms for customers attracted over 1.2 billion users worldwide (20% of the world’s population). In Brazil, credit card penetration is even higher: 80% of Brazilians have credit cards issued to them.

Despite high penetration, credit cards have remained largely unchanged (offering similar conditions and experiences globally) and failed to adapt and meet the purchasing needs of thousands of Brazilians.

This standardization prompted non-financial entities to enter the market. Private Label Cards and "crediário" (recently denominated BNPL) emerged in Brazil during the 1950s as a retail-led strategy to drive sales. Major retailers recognized that providing customers with credit lines and installment payment options facilitated their ability to make purchases. Over the past 70 years, this sector has evolved into one of Brazil's most significant and lucrative financial services, with nearly 50% of Brazilians utilizing in-store credit solutions.

Credit cards, processing fees and Private Label Cards / “crediário” combined have a revenue pool of $40.1 billion.

1. POS Lending: store cards and Point of Sale credit. Paid by Brazilian Consumers in 2021.

2. Processing Fees paid by Brazilian merchants in 2021

Why now:

UME was born from the conviction that we live in a unique historical moment to build the next generation of payment networks in Brazil. Over the last few years, some tailwinds have made the market favorable to rethink these networks:

1. In 2020, the Brazilian Central Bank launched Pix, an instant payment system that allows users to make payments and money transfers instantly, 24/7, with little or no cost. Since it was introduced, Pix adoption has skyrocketed making it the most popular payment and transfer method in Brazil, surpassing debit, credit cards and bank transfers, with TPV reaching R$ 11T in only 2 years.

2. During the pandemic, SMB merchants have become more connected and seek products that improve their bottom line.

3. The high penetration of cell phones allows for online transactions without needing a card.

Pix has transformed the Brazilian financial landscape by promoting faster, more accessible, mobile payment transactions. Although Pix transactions are primarily debit transactions, credit products (such as Pix Parcelado and Pix Garantido) are outlined in the Central Bank’s Pix roadmap.

Solution:

UME aims to leverage the growing popularity of digital payments by establishing a closed-loop network on the Pix infrastructure, offering a superior alternative to traditional credit cards and payment networks. UME connects retailers and consumers by providing users with a credit facility for making installment purchases through Pix transactions.

Customers can apply for a credit limit at any of UME's partner stores, taking less than five minutes to complete. Once approved, customers can utilize their credit limit to make purchases from retailers within the UME Network. Retailers in the UME Network have experienced revenue growth of up to 15%.

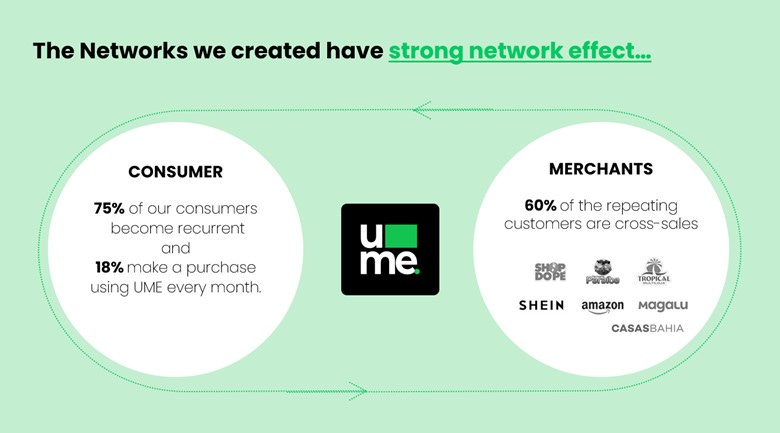

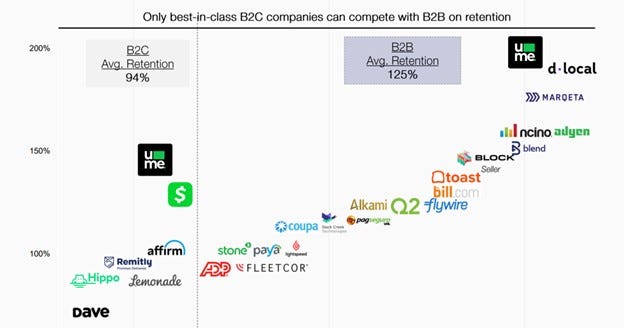

Building network density has proven crucial to UME’s success. With a regional, city-by-city go-to-market strategy targeting first offline merchants and expanding the offer to the e-commerce, UME has been able to create networks with strong network effects that lead to world class Net Dollar Retention:

Source: Coatue whitepaper – Fintech and the Pursuit of the prize. Who stands to Win Over the Next Decade

Since 2020, UME’s execution has proven their initial convictions right. They have gone from zero to more than 150,000 consumers, +1,000 stores, and 15% of the active population in our initial hub. The high density of the UME Network leads to high repeating rates (% of repeating purchases over time by hub).

What’s next:

UME’s potential is enormous: currently their operation is concentrated in regions that represent less than 4% of the Brazilian population, indicating vast untapped opportunities for expansion and reaching a much larger customer base.

Founders:

Berthier Ribeiro - CEO, co-founder

Theo Ramalho - COO, co-founder

Marco Cristo,PHD - Head of Data Science, co-founder

Investors:

NFX, Canary, Big Bets, Clocktower Ventures and Norte Ventures.

Given the rapid rise and success of UME, how do you see traditional credit card companies responding to this new business model and what strategies do you believe they might employ to effectively compete in this new landscape of digital payments?