LatAm Tech Weekly

238: SPECIAL EDITION: ENTERPRISE AI & THE ORCHESTRATION LAYER

Weekly writing about what is happening in LatAm tech. By day, I am part of the corporate development team at Itau Unibanco. By night, I am reading and learning about technology in general (now, with a focus on AI). During the weekends, I’m writing the LatAm Tech Weekly. And obviously, always running!

If you have not subscribed yet, join the 14,700+ weekly readers by subscribing here!

Happy Sunday!

It’s been a while since I last sat down for a truly deep read of some of the best papers being published out there. I know these editions tend to be denser, but I also know many of you genuinely enjoy this format — I certainly do. If you’ve been following me for a while, you know I live in this interesting contradiction: on one hand, I’m an extremely heavy AI user; on the other, I still love doing certain things “the old-fashioned way.” For reports that I know are truly worth my time, I print them out, grab a highlighter and a pencil, and go through them page by page — reading, reflecting, taking notes, and ultimately building my own synthesis and takeaways.

And this week’s read absolutely deserved that treatment (over 300 pages read!)

In fact, it was so good that I decided to dedicate an entire special edition to it. So if you’re into AI (which, at this point, you probably should be), keep reading. If not, feel free to jump straight to the news section. Without further ado, let’s dig in!

PS: The piece is very long, if your provider has limitations and you cannot see it as a whole, go to: juliadeluca.substack.com

The Orchestration Layer: A Special Edition

On Raphaëlle d’Ornano’s Orchestration Economics Manifesto — and what Gartner confirms, complicates, and misses.

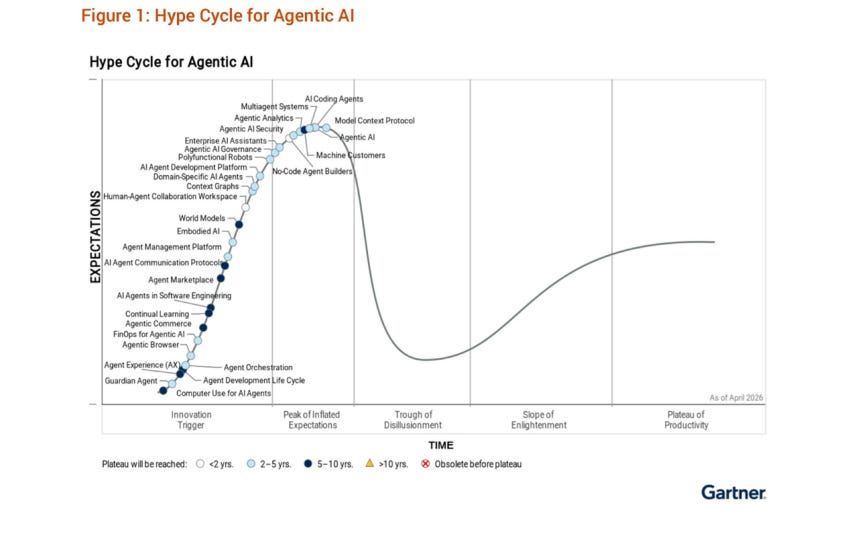

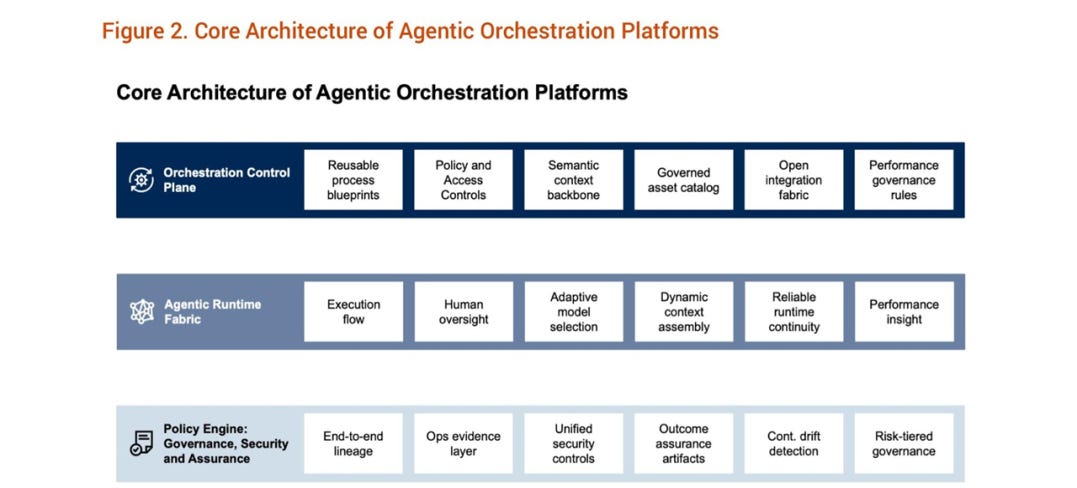

This week I read three documents that, taken together, form the clearest picture I’ve seen yet of where enterprise AI is actually going — and more importantly, who captures the value when it gets there. The first is Raphaëlle d’Ornano’s The Orchestration Economics Manifesto (AGNT, Spring 2026), a capital-allocation thesis written with the kind of conviction that either ages very well or very badly. The other two are Gartner’s Hype Cycle for Agentic AI (April 2026) and AI Vendor Race: Enterprise AI Will Fail to Scale Without Agentic Orchestration Platforms (January 2026) — drier, more cautious, written for enterprise procurement committees rather than investors.

They don’t agree on everything. But they triangulate on the same fault line running beneath the technology economy right now: the battle for the Orchestration Layer. And the question none of them quite answers cleanly — but that d’Ornano gets closest to — is the one with the most money riding on it: who actually captures the economic surplus of this transition?

That’s the question I want to work through here. I’ll follow d’Ornano’s framework, since it’s the sharper instrument, and bring in Gartner where it confirms, complicates, or catches something she misses.

The Discontinuity

Let’s start with d’Ornano’s central claim, because it’s the one everything else depends on. She argues that what’s happening with generative and agentic AI is not a disruption — it’s a discontinuity. The difference is the following: disruption changes the slope of a curve: cloud computing was disruption, because it was the same CRM or payroll software, just differently priced and delivered. A discontinuity breaks the curve entirely. Something so fundamentally new arrives that most existing mental models don’t just become less useful — they become obstacles.

The shift she’s describing is this: for the entirety of the digital age, software processed instructions. A human decided what to do, selected a tool, and directed its operation. The tool accelerated the human’s work. It did not perform it. The human remained the unit of production. And, if you have been following along, with AI this architecture is over.

For the first time, software receives goals, decomposes them into tasks, selects its own tools, executes autonomously, and delivers outcomes. A team of AI agents is not a faster tool it is a new kind of economic actor.

The evidence is already in market data. By April 2026, more than $2 trillion had been wiped from software market capitalization in twelve months — the worst decline in over thirty years. A single product announcement from Anthropic in February 2026 (plugins for a niche agentic workspace) triggered $285 billion in repricing in 48 hours. The sell-off affected sectors that t were supposed to be impermeable: software on Monday, wealth management on Tuesday, commercial real estate on Wednesday, logistics on Thursday, insurance on Friday. Five sectors in five days, following a logic that no standard analytical framework was built to articulate.

Six Tremors, One Fault Line

How did we get here so fast? D’Ornano identifies six rapid phase shifts between September 2024 and early 2026 that, taken individually, each looked significant. Together, they produced something that hadn’t previously existed.

1. Intelligence arrived: OpenAI’s o1 crossed the PhD reasoning threshold. It scored 77.3% on GPQA Diamond, a benchmark of graduate-level science questions where human PhD experts score 69.7%. By early 2026, multiple models from competing laboratories exceeded 90%.

2. Intelligence became accessible: DeepSeek demonstrated that near-frontier capability could be achieved at 20–50x lower cost than OpenAI’s leading model. By August 2025, a hybrid model delivered roughly 90% of GPT-5’s capability at 1–2% of the cost. (Quick definition for context: “frontier model” just means the most capable AI model available at a given moment. When DeepSeek matched the frontier at a fraction of the price, it meant intelligence stopped being a luxury good.)

3. Silicon independence: Google’s Gemini 3 Pro achieved the strongest frontier performance available trained entirely on non-NVIDIA chips. The implication: frontier AI no longer required NVIDIA’s monopoly on the hardware that makes it run, which had been the assumption structuring most of the investment thesis in the space.

4. Protocol standardization: Anthropic’s Model Context Protocol (MCP) became the TCP/IP of the Agentic Era — a universal standard for how AI agents connect to external services, use tools, and maintain context across interactions. (Think of it like USB: before USB, every device had its own connector. MCP is the moment AI agents got a universal plug.) Within twelve months of launch, it surpassed 97 million monthly SDK downloads and was adopted even by OpenAI and Google.

5. The Inference Swarm: Moltbook, a Reddit-like platform for autonomous agents, saw 1.5 million agents register within days of launch — generating millions in daily compute spending without human attention. Agent populations, unlike human populations, can double in days.

6. The Long-Context Frontier: Models began holding entire codebases — millions of tokens — in working memory, enabling sustained autonomous engineering rather than assisted editing. (A “token” is roughly a word or word fragment; “long context” means the model can hold an entire large codebase in mind at once, the way a senior engineer might, rather than only seeing small snippets at a time.)

Together, these six shifts produced something that had not previously existed: intelligence that is cheap, ubiquitous, coordinated at machine scale, and accessible to anyone with an API key.

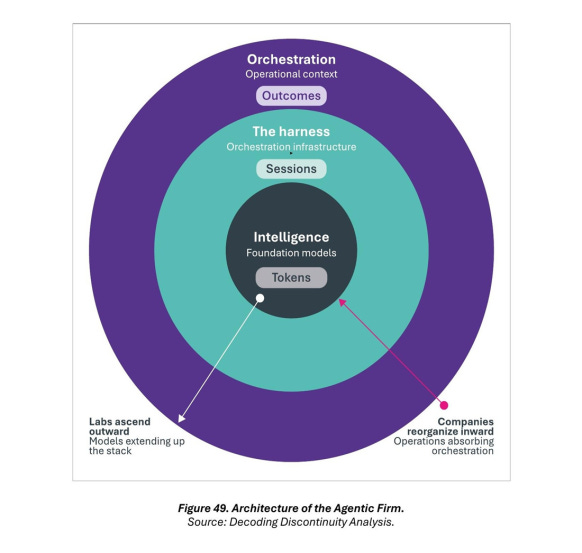

The Three-Ring Architecture

When machines become actors, someone must direct them. D’Ornano’s framework organizes the Agentic Era company into three concentric rings — and the economic logic of each ring is radically different.

Ring 1 — Intelligence: The foundation models that provide cognitive capability — GPT, Claude, Gemini, and the rest. They are converging, commoditizing, and available from multiple providers at near-parity. The economic unit here is the token. You pay per word, essentially, and the price is collapsing.

Ring 2 — The Harness: The orchestration infrastructure that makes intelligence operational: decomposing goals into tasks, delegating to specialist agents, managing state, coordinating execution. Claude Code, Cowork, OpenAI’s Frontier are all Harness products. The economic unit is the session. This is where a lot of the current AI product market lives — and where, d’Ornano argues, the moats are thinner than they look.

Ring 3 — The Orchestration Layer: This is where value is captured beyond the AI labs. The entity that places intelligence and the Harness at its core, then adds what neither can produce — irreplaceable operational context accumulated through actually running the world — holds the position d’Ornano calls AGNT. The economic unit is the outcome.

The software company with millions of CRM execution patterns. The insurer that has adjudicated ten million claims. The carrier that has routed a billion shipments. The bank that has underwritten a trillion dollars in credit. Each possesses operational reality that no model can synthesize from training data and no Harness can accumulate from orchestrating sessions. That context is the irreplaceable asset of the Agentic Era.

Gartner’s AI Vendor Race paper describes the same architecture with different vocabulary — a control plane, a runtime fabric, a policy engine — but arrives at an identical conclusion: the entity that unifies intent, execution, and verification into a governed system of action is where platform value concentrates. The language is drier. The point is the same.

The Three Laws

D’Ornano then gives you a scoring system, three structural conditions that determine whether an orchestration position is durable. This is the most useful part of the manifesto, because it lets you run any company through the test.

Law 1: Proximity to Intent Captures Value- The orchestrator must sit where the human’s goal originates. Whoever owns that moment controls routing, and routing is the mechanism of value capture. Downstream tools become interchangeable. Upstream positions become irreplaceable. Moats no longer form where data sits. They form where intent originates.

Law 2: Context Builds Moats- Data alone does not create competitive advantage. Context does. Data tells you what happened. Context tells the agent what to do next. The insurer that has processed ten million claims possesses operational intelligence that no foundation model can synthesize from training data alone. This context compounds with every interaction. A competitor can license the same models. It cannot manufacture the memory of ten thousand orchestrated workflows.

Law 3: Workflow Intelligence Secures Control- The orchestrator’s coordination patterns must improve with use. The system that has processed fifty thousand claims handles the fifty-thousand-and-first differently from a new entrant seeing its first. The orchestrator learns which specialists work well together, which sequences minimize error, which exceptions require escalation — what d’Ornano calls meta-expertise. It creates switching costs that strengthen, not decay.

She’s honest that Law 3 is the weakest of the three because pure workflow choreography is increasingly learnable by capable agents. Context, she says, remains the ultimate foundation of defensibility. Gartner adds something important here that d’Ornano leaves implicit: the next competitive dimension isn’t just holding context, it’s proving outcomes. Enterprises are shifting to platforms that can verify results end-to-end, with transparent evidence of performance, compliance, and cost control. Governance-as-product, not governance-as-feature. That’s a harder thing to build than a context moat — and it’s where most of the current field is still falling short.

Satisfy all three laws, and you hold a compounding, hard-to-bypass position that captures the economic surplus of abundant intelligence. Satisfy one or two, even brilliantly, and you are the most valuable crew member on someone else’s ship.

Captain and Crew

This is d’Ornano’s most clarifying metaphor, and I keep coming back to it. In a multi-agent system, a master agent coordinates a crew of specialists. The specialist agents are valuable because they have real reasoning capacity. But they are no longer where the workflow is decided. Their job is to respond to the plan, not define it. And they are substitutable… A better pricing model can replace the incumbent. A better extraction agent can be swapped in. The crew is upgradeable. Its members have limited pricing power because the captain can always source a better one.

The captain is not substitutable. Replacing the orchestrator means rewiring the workflow — remapping the topology, reestablishing every integration, re-accumulating operational memory. The switching cost is categorical.

This has a direct implication for the most debated question in enterprise software right now. The sell-off that followed Anthropic’s plugin announcements treated Thomson Reuters and ServiceNow as though they faced the same threat. They do not. Thomson Reuters monetizes cognitive arbitrage — a comparison and synthesis function that agents now perform at a fraction of the cost. ServiceNow holds the operational workflow layer for IT service management across 8,800 enterprise customers, with 98% renewal rates and workflow control that the Three Laws identify as the foundation of orchestration value. The undifferentiated panic created one of the most significant mispricings in recent market history.

The Palantir Test

The manifesto applies the Three Laws directly to Palantir, which makes for one of its best sections. Palantir is exactly the kind of company that looks like an AGNT until you run it through the framework carefully. Palantir’s market cap sits at $307 billion as of mid-April 2026, with 70% year-over-year revenue growth accelerating for the tenth consecutive quarter. The execution is genuinely extraordinary.

It passes Law 2 — context depth — with distinction. Its Ontology is a programmable operational model of the enterprise: it maps real-world objects to digital objects with defined properties, relationships, and executable actions. It is not a database nor a semantic layer. The closest analogy is an operating system for enterprise operations.

It conditionally passes Law 3 — workflow intelligence — within its deployments. The Ontology defines what agents are permitted to do, constraining and governing their actions across entire enterprises.

But it fails Law 1 — proximity to intent. No user opens Foundry to express a business goal. Intent capture happens elsewhere — and the orchestrator who captures intent controls routing. The Ontology is indispensable within the workflow. But the orchestrator decides whether the workflow runs at all, and whether it routes through the Ontology or around it. Indispensable is not the same as orchestrator.

The stock trades at 67x trailing revenue — priced as the orchestrator of the agentic economy, the company that will direct the work. The architecture describes a company that governs the work once directed. The distance between those two positions is measured in hundreds of billions of dollars. The Ontology is the most valuable crew member on the ship. But, it is still crew.

The Software Sorting

The February 2026 sell-off was directionally correct and analytically lazy. What is actually happening is not the death of SaaS (or SaaSpocalypse that I have mentioned several times here) it is what d’Ornano calls the Software Sorting: a structural re-ranking of where control, coordination, and value will reside when autonomous agents become the primary actors inside enterprises. The greatest carnage, according to the paper, will fall on “workflow wrappers”: AI application companies built on the thesis that there would be a durable margin between what a foundation model could do and what an enterprise needed done. Anthropic demonstrated that this gap closes at the speed of a plugin built in weeks. The common vulnerability: if your product is “model + wrapper + workflow” and the model creator can ship the wrapper as a plugin, the moat was never structural. It was temporal.

Gartner’s Hype Cycle has a useful name for the noise obscuring this: “agent-washing” which are legacy automation tools rebranded with the vocabulary of agency. Only 17% of organizations have actually deployed AI agents so far, with 42% expecting to do so in the next 12 months — the most aggressive adoption curve Gartner has tracked across any emerging technology. But 70 to 80% of agentic initiatives haven’t made it to enterprise scale. The gap between what’s being sold and what’s being deployed is wide. This is the hype-versus-reality tension that d’Ornano’s framework is designed to cut through: not all AI activity is orchestration, and the distinction matters enormously for where value ends up.

The so called “systems of record” — Salesforce, ServiceNow, Workday, SAP — face a different and more nuanced challenge. Ripping them out isn’t about switching to a cheaper plugin. It means migrating decades of operational data, retraining thousands of users, rebuilding integrations across dozens of downstream systems. But their economic role is being renegotiated. The question is whether they remain “systems of action” — the layer that receives intent and directs agents — or are demoted to “systems of storage”: the database behind someone else’s orchestrator. The distinction determines whether they trade at 3x revenue or 15x revenue.

One counterintuitive data point worth holding onto: the model layer is architecturally the most substitutable component in the entire stack. Only 11% of enterprise builders switched AI providers in the prior year — not because of technical lock-in, but because of organizational complexity. A CRM that holds fifteen years of customer data requires two years and $50 million to migrate. An LLM can be swapped by changing an API endpoint. LLM lock-in is real, but fundamentally more fragile than data lock-in.

The Market Right Now

ServiceNow is down 41% year-to-date. Salesforce is down 36%. The market is, clumsily and probably excessively, pricing in displacement risk — the fear that AI agents could route around the software layer entirely. D’Ornano calls this “bypass risk”: the scenario where the orchestration layer doesn’t flow through incumbent software but circumvents it entirely.

The Gartner Hype Cycle frames the same phenomenon more neutrally: the shift from native applications to “agentic front ends”, where instead of a CRM with a built-in agent, organizations assemble ecosystems where agents from different vendors coordinate through shared protocols like MCP and A2A. (A2A — Agent-to-Agent — is a competing protocol to MCP, essentially a different proposed standard for how AI agents talk to each other. The protocol wars between MCP and A2A are, in infrastructure terms, the equivalent of the VHS vs. Betamax moment of this transition.)

The analogy to the microservices transition is right — value migrated away from monolithic applications to the orchestration layer that connected them. The question is whether Salesforce and ServiceNow are Oracle circa 2005: dominant but structurally exposed, or whether they successfully become the orchestration layer themselves.

The d’Ornano answer is that this depends on the Three Laws test. Salesforce acquired Informatica and launched Agentforce — moves that are, in her terms, attempts to deepen context and claim proximity to intent. Agentforce ARR reached $800 million, up 169% year over year. Whether that constitutes genuine orchestration layer control or expensive repositioning that’s still one abstraction too far is the investment question, and it’s genuinely open. ServiceNow’s CEO has called the company “the AI control tower for business reinvention” — the language is d’Ornano’s language, whether or not it’s her framework.

What neither company has fully demonstrated is the element Gartner identifies as decisive going forward: governance-as-product. Not a compliance checkbox, but provable, auditable, outcome-indexed performance that enterprises can defend to stakeholders and regulators. That’s a harder thing to build than a rebrand and it’s where the next phase of the sorting will be decided.

The Leviathans Ascend

This is d’Ornano’s most counterintuitive claim, and I think it’s also her most important one: the largest value creation of the Agentic Era may not occur in companies building AI. It may occur in the companies that use it — the industrials, financials, insurers, healthcare systems, and consumer platforms that constitute the majority of the S&P 500 and have never been considered technology plays.

For a generation, markets rewarded asset-light business models. The freight broker without trucks traded at higher multiples than the carrier. The wealth platform that held no assets was valued more than the bank. The logic was simple: in a knowledge economy, cognitive capital outperforms physical capital. Brains beat iron.

Agentic AI inverts this: If cognition becomes abundant, cognitive capital loses its scarcity premium. What remains scarce is operational context — the accumulated intelligence generated by actually running a business over time. The logistics carrier’s knowledge of lane pricing dynamics, seasonal patterns, and equipment failure modes across every corridor it serves. The insurer’s actuarial loss data built over decades of underwriting real risk with real capital. A bank’s century of credit decisions with outcomes observed.

This context is not data in a warehouse. It cannot be replicated from public sources. You cannot simulate decades of clinical trial outcomes. You cannot reconstruct the institutional understanding of a logistics network from its transaction logs, any more than you can reconstruct a surgeon’s judgment from operating room medical records. The records document what happened. The judgment is the product of having been there, every day, for ten thousand cases.

Two forces follow from this inversion:

Reinternalization — where the asset owner deploys agents to recapture margin previously paid to cognitive intermediaries. An insurer who deploys its own agents reinternalizes the distribution function, converting broker commissions (typically 5–15% of premium) into margin. For a global insurer writing $30 billion in annual premium, that arithmetic is immediate.

The Meta-Layer — where the asset owner deploys its operational intelligence as agents operating inside its customers’ infrastructure, creating entirely new revenue lines that did not exist before the agentic transition. A construction equipment manufacturer deploys coordination agents on customers’ job sites, optimizing equipment utilization in real time. The manufacturer is no longer selling machines. It sells construction orchestration as a service. The hardware becomes nodes in an intelligent network. The Orchestration Layer becomes the margin.

The Embedded Option

Every company in the agentic economy carries two possible futures inside a single stock price. D’Ornano calls them two value curves:

The Fundamentals Curve — the company as it exists today, growing at its current trajectory, valued by every DCF model and comparable screen in active use. (DCF — discounted cash flow — is the standard financial model for valuing a company: roughly, what are all future cash flows worth in today’s dollars.)

The Orchestration Curve — the company after the crossing, delivering outcomes priced against the labor budget, compounding coordination intelligence with every workflow processed.

The gap between these two curves is an embedded option. And it runs in both directions. The negative option exists in companies whose structural moat is already eroding beneath an income statement that hasn’t yet registered the damage. Revenue is growing. Retention is stable. Margins are healthy. The DCF looks sound. But the architectural position, as measured by the Three Laws, has already deteriorated. The moat broke. The revenue will follow. The instruments will detect the break only when it arrives as a financial result — by which time the negative option has already been exercised against shareholders.

The positive option exists too — but it resolves later. Building the Orchestration Layer requires accumulating context across thousands of workflows, proving reliability, earning institutional trust. The financial signatures emerge gradually, quarter by quarter.

The destruction was priced in days. The creation will be priced in years.

In my humble opinion, this temporal asymmetry isthe most actionable insight in the manifesto. It explains why the current market moment is so disorienting — the negative options are resolving fast and visibly, while the positive ones are still invisible in the data.

The Sorting Arithmetic

Of the 391 S&P 500 companies exposed to the agentic transition, d’Ornano’s ARAF™ framework — Architectural Resilience Assessment Framework — sorts them into six structural positions:

1. Context Prisoners (167): Companies with extraordinary operational context trapped in legacy architecture. The widest embedded option in the market, but the most urgent challenge.

2. Platform Defenders (91): Companies that already possess both context depth and technical readiness. Payment networks, enterprise software platforms, financial data companies. The most contested ground in the economy.

3. Ascending Tools (31): Technically excellent companies demonstrably moving up the stack — acquiring context, constructing intent surfaces.

4. Tool Layer (46): Technically excellent but structurally mispositioned. API-first, agent-compatible — and competing on price for a function call.

5. Emerging Orchestrators (19): High layer position, high technical readiness, building the position rather than defending an inherited one.

6. Vulnerable (37): Workflow wrappers or cognitive intermediaries. Thin applications one model-provider plugin away from irrelevance.

What the Gartner Papers Add

D’Ornano’s manifesto is the sharper instrument, but the two Gartner papers add something she doesn’t linger on: friction. The Hype Cycle is particularly honest about the gap between what’s being sold and what’s being deployed. Gartner estimates that more than 40% of agent projects will fail by 2027. Fully autonomous agents are not ready for most enterprise use cases. And “agent-washing” is actively muddying the market — making it harder for enterprises to distinguish genuine orchestration architecture from rebranded workflow automation.

There’s also a broader point the three documents together illuminate that none of them quite names directly: we are in the middle of a legitimacy crisis for existing analytical frameworks. D’Ornano opens her manifesto by arguing that the conventional tools built to navigate the last regime are obstacles to surviving the next one — that disruption theory, which assumes incumbents can be mapped against an S-curve, misses the nature of a discontinuity. The Gartner papers operate more cautiously within established frameworks, which is both their strength and their limitation. The Hype Cycle format assumes technologies move through predictable phases from peak inflated expectations to a trough of disillusionment toward a plateau of productivity. That model may not hold when the underlying economic structure is changing underneath every company simultaneously. You can’t plot a hype cycle for a transition that resets the coordinate system.

What we’re watching in the market — the software selloffs, the governance debates, the protocol wars between MCP and A2A, the nuclear power deals Microsoft and Google are signing to keep data centers running — is the infrastructure phase of a platform transition. And platform transitions have a well-established historical pattern: the first phase looks like chaos, the second phase produces a few winners who control the coordination layer, and the third phase involves everyone else paying rent to those winners. The internet produced Google and Amazon this way. Mobile produced Apple and the app store model. D’Ornano is arguing, with considerable analytical support, that the agentic transition will produce its own coordination layer controllers — the AGNTs — and that they will be neither the model labs nor the legacy SaaS vendors, but the companies that manage to be simultaneously close to institutional intent, rich with irreplaceable operational context, and intelligent about workflow.

The open question — and it’s the one that keeps this from being a settled debate — is timing. D’Ornano’s cost collapse trajectory ($100 to $10 to $1 to pennies over three years) is a forecast. And forecasts about the pace of technological change have a long history of being approximately right in direction and dramatically wrong in speed. The gap between the infrastructure being built and the outcomes being reliably delivered is still wide enough that the companies who can bridge it — who can turn the orchestration promise into auditable, governed, measurable production — haven’t yet fully revealed themselves.

That’s the embedded option. The gap between what’s being built and what’s been proven. What makes this moment so difficult and so interesting to navigate.

We are only in the very earliest days of this new paradigm. But we can give it a name: Orchestration Economics. The companies who capture the Orchestration Layer will emerge from the discontinuity stronger than the systems that preceded it. Others will fracture under the same forces. We don’t yet know all the rules.

But the discontinuity is real. We know enough to begin.

General news:

• Itaú Unibanco integrated generative AI into its new “laranjinha+” payment terminal, enabling merchants to process payments through voice commands directly on the POS device. The feature turns the terminal into an AI-powered sales copilot designed to simplify operations, reduce errors and accelerate transactions without additional hardware or changes to security protocols. 🇧🇷

• Klarna returned to profitability in Q1 2026, posting $17M in profit with revenue surpassing $1B and GMV reaching $33.7B. The results reinforce continued expansion of the BNPL market amid strong consumer adoption in the U.S. 🇸🇪

• Jeeves launched operations in Argentina and appointed Federico Javin to lead its stablecoin strategy as it targets over $500M in annualized processing volume. The fintech is betting on Argentina’s rapid adoption of digital dollars and crypto-based financial infrastructure. 🇦🇷

• Banco do Brasil is expanding its CVC strategy with two new funds totaling over R$250M focused on fintechs, agtechs, govtechs and ESG startups. The bank aims to deepen startup integration and increase exposure to later-stage investments. 🇧🇷

• Erebor Bank started talks to reconnect Venezuela to the U.S. financial system after a partial easing of sanctions. Backed by Peter Thiel, the digital bank is proposing correspondent banking services and U.S. subaccounts for Venezuelan clients. 🇻🇪

Deals:

• Capim acquired Dental Office in a transaction that also marks an exit for Stone as it restructures its startup portfolio. The deal expands Capim’s reach to more than 12,000 dental clinics by integrating clinic management software with financing and payment solutions. 🇧🇷

• Z.ro Global Payments acquired Paag’s payments division to strengthen its position in the iGaming and online betting market. The acquisition pushes the company beyond 500M processed transactions and creates a dedicated gaming-focused payments unit. 🇧🇷

General news:

• SpaceX’s anticipated IPO could become one of the biggest VC paydays in history, potentially valuing the company between $1.75T and $2T. The offering could raise up to $80B while consolidating AI, Starlink and aerospace operations under Elon Musk’s broader ecosystem. 🇺🇸

• WideLabs is raising a $50M Series A to scale its AmazônIA LLM platform across Latin America. Backed by NVIDIA, Oracle and AWS, the startup is positioning itself as a sovereign AI infrastructure provider focused on regional languages and enterprise solutions. 🇧🇷

• Lulo X launched tokenized gold through Pax Gold (PAXG), becoming the first digital banking app in Colombia to offer tokenized physical gold trading. The initiative strengthens the trend of combining traditional assets with crypto infrastructure for wealth preservation. 🇨🇴

• Brazil’s Senate approved the creation of a parliamentary front focused on startups and innovation aimed at improving legal certainty, expanding access to capital and strengthening entrepreneurship policies. The initiative seeks to deepen coordination between lawmakers, universities and the startup ecosystem. 🇧🇷

Deals:

• Pitz raised an additional $2.9M, bringing total funding to $5M in less than a year. The AI-powered platform digitizes auto repair shops through diagnostics, logistics and management tools and plans to expand into the U.S. by year-end. 🇧🇷

• SolarZ raised R$5.8M in a round led by Triaxis Capital and Crescera Capital to expand its fintech and software solutions for solar energy integrators. The company serves more than 6,000 clients and plans deeper integration of AI and financing products. 🇧🇷

• Banco BS2 spun off its capital markets operations into BBS Capital Partners, creating an independent platform focused on private credit, FIDCs and structured capital solutions. The new company starts with over R$1.2B in assets under management. 🇧🇷

General news:

• Brazil’s government issued new decrees expanding obligations for digital platforms following a Supreme Court ruling that platforms can be held liable for systemic failures in removing illegal content. The measures increase requirements around fraud prevention, AI-generated harmful content and online violence while strengthening oversight by Brazil’s data protection authority. 🇧🇷

• Zendesk announced a $100M investment to expand Zendesk for Startups, extending benefits to venture capital firms and startup ecosystems globally. The initiative offers free access to AI agents, onboarding support and partnerships with platforms such as AWS, GitHub and Notion. 🌎

• inDrive launched Aurora Ventures, an investment initiative focused on women-led startups across Latin America, Africa and the Middle East. The program plans to invest up to $250K per startup while providing mentorship and operational support. 🌎

• iFood filed a lawsuit against Keeta and Meituan accusing the companies of unfair competition and corporate espionage in Brazil. The case involves allegations of payments for confidential information related to operations, logistics and investment plans. 🇧🇷

• SpaceX officially filed for its IPO, targeting a valuation above $1.5T and aiming to raise at least $80B. The filing revealed $18.7B in 2025 revenue driven mainly by Starlink, while continued investments in AI and infrastructure pushed the company to a net loss. 🇺🇸

Deals:

• Draiven raised R$3M led by Asterismus Capital and acquired Rabt Automation to expand its AI-driven corporate decision-making platform. The acquisition adds workflow automation and low-code execution capabilities as the company accelerates expansion into the U.S. and Europe. 🇧🇷

• Checker raised $8.1M in a seed round led by Galaxy Ventures, Al Mada Ventures and Framework Ventures to scale its stablecoin and API-based payments infrastructure across Latin America. The company plans to integrate AI agents into treasury and financial operations. 🌎

• Mercury raised $200M in a Series D led by TCV, reaching a $5.2B valuation. The fintech serves more than 300,000 customers and plans to expand AI-powered financial products while pursuing a U.S. banking charter. 🇺🇸

General news:

• Anthropic told investors it expects to post its first operating profit sooner than projected, potentially putting the company ahead of OpenAI on profitability. The AI startup generated $4.8B in Q1 revenue, driven largely by coding products such as Claude Code, reinforcing pressure for sustainable economics across the AI sector. 🇺🇸

• Abroad launched EchoPay, an interoperable QR payment device that confirms transactions through real-time audio validation. The solution aims to reduce fraud and simplify in-person payments as the company expands across markets including Brazil, Colombia, Vietnam and the Philippines. 🌎

• The IPOs of SpaceX, OpenAI and Anthropic could trigger major capital rotation on Wall Street as new Nasdaq rules accelerate index inclusion for newly listed mega-cap companies. Analysts estimate passive funds may need to reallocate tens of billions from existing tech holdings. 🇺🇸

• Zavii plans to invest R$20M in new startups after launching ventures across fintech, healthtech and consumer brands. The venture builder is expanding its “building as a service” model with new businesses focused on fitness payments and protein products. 🇧🇷

• Cobre is expanding digital cross-border payments in Latin America as instant payment systems like Pix and SPEI accelerate adoption. The fintech is positioning itself around B2B payments infrastructure and stablecoin-driven financial operations. 🌎

• The Federal Reserve proposed restricted “master accounts” for fintechs and crypto firms, potentially giving nonbank players direct access to U.S. payment infrastructure. The move could accelerate fintech and crypto integration into the financial system. 🇺🇸

• Banco Central do Brasil updated FX reporting rules for cryptocurrency transactions, reinforcing oversight of cross-border crypto payments and transfers. The update aligns with Brazil’s broader digital asset regulatory framework. 🇧🇷

Deals:

• Robbin raised an $8M seed round co-led by Canary, Atlântico and Caravela to expand its AI-native credit and payments platform for retailers and suppliers. The company also structured a $100M FIDC to finance operations through 2027. 🇧🇷

• Evertec is acquiring a majority stake in BBChain through a two-phase deal starting with a R$28M investment for 67% ownership. The acquisition strengthens Evertec’s push into blockchain infrastructure and tokenization across Latin America. 🇧🇷

• Memed raised an R$80M round co-led by DGF and BridgeOne to expand AI integration into clinical workflows and prescription infrastructure. The healthtech expects to surpass R$100M in revenue in 2026. 🇧🇷

• MSW Capital launched BB Ventures 2 with R$115M in committed capital focused on fintech, agritech, govtech and AI startups. The new fund expands the firm’s strategy into selective Series B investments. 🇧🇷

• Sinatra AI raised R$10M in a seed round led by BluStone to expand its AI platform for detecting pricing errors, fraud and operational anomalies in e-commerce. The startup already serves clients such as Americanas and Decathlon. 🇧🇷

• Palenca raised $4M in a round led by Experian to expand its income verification and credit infrastructure platform. The fintech connects lenders to private employment data and plans to develop new AI-driven predictive models. 🇲🇽

General news:

• Hyperliquid launched perpetual Ibovespa contracts with up to 20x leverage, expanding its crypto-native derivatives offering beyond Bitcoin, gold and the S&P 500. The platform processes around $8.5B daily with only 12 employees, reinforcing how blockchain infrastructure is advancing into traditional financial markets. 🌎

• France announced over €1B in new investments for quantum computing alongside an additional €550M for microelectronics, intensifying global competition for post-AI technologies. The move follows a recent $2B U.S. investment initiative in quantum startups and infrastructure. 🇫🇷

• Flair partnered with Copec to scale its AI-powered HVAC optimization technology in Chile. The platform reduces air conditioning energy consumption by up to 40% without requiring hardware replacement, targeting corporate and industrial clients. 🇨🇱

• VendeX will launch its second edition in July, offering a virtual revenue acceleration program for startups and SMEs across Latin America. The initiative combines AI tools, sales optimization and operational execution for companies generating up to $6M annually. 🌎

• Grupo Alun launched Lumina, an AI platform integrating more than 55 specialized agents across functions such as HR, sales, marketing and product management. The company aims to reach R$100M in revenue by 2030 while positioning itself as a governed AI environment for enterprises. 🇧🇷

• The U.S. government announced a $2B investment program in quantum computing, including $1B allocated to IBM for a quantum chip manufacturing facility in New York. The initiative strengthens domestic semiconductor and quantum infrastructure capabilities. 🇺🇸

Deals:

• DIO Inteligência raised R$4M in a seed round led by Triaxis Capital and Crescera Capital to expand its AI-powered dental diagnostics platform. The startup analyzes radiography images in seconds and plans to grow beyond clinics into insurance audits and predictive analytics. 🇧🇷

• Mozart raised a $600K pre-seed round led by Orbit Ventures to scale its AI-powered debt collection platform across Brazil and Mexico. The company serves over 50 clients with conversational AI agents that negotiate with debtors in real time. 🇺🇾

One of the most important AI developments this week was the news — first reported by Reuters and later reinforced by the Financial Times and The Wall Street Journal — that leading AI labs are beginning to show signs of real profitability at scale. Anthropic is reportedly on track to post its first profitable quarter, with projected Q2 2026 revenue of $10.9B and an operating profit of roughly $559M, driven largely by explosive enterprise demand for Claude and AI coding agents. At the same time, OpenAI is accelerating IPO discussions as revenues continue to surge, while investors increasingly focus on whether frontier AI can evolve from a capital-burning experiment into a sustainable business. This matters because one of the biggest criticisms of the AI boom has always been the lack of a clear path to monetization given the massive infrastructure and compute costs involved. If frontier labs begin demonstrating profitability — even temporarily — it fundamentally changes the narrative around AI from “hype cycle” to a potentially durable new platform shift. It also helps justify the unprecedented levels of capital flowing into the sector, from trillion-dollar infrastructure ambitions to record venture rounds, while likely accelerating even more investment, competition, M&A, and IPO activity across the global AI ecosystem.

RIO2C 2026

Date: May 26–June 1, 2026

Location: Rio de Janeiro, Brazil

Description: A creativity-driven event connecting technology, media, audiovisual, music, sustainability, and entrepreneurship.

More infoSouth Summit Madrid 2026

Date: June 3–5, 2026

Location: Madrid, Spain

Description: A global innovation conference connecting startups seeking scale with investors and corporations looking for new opportunities.

More infoMoney20/20 Europe 2026

Date: June 2–4, 2026

Location: Amsterdam, Netherlands

Description: One of the world’s leading fintech and financial services conferences, gathering global banks, fintechs, investors, regulators, and technology companies to discuss the future of payments, banking, AI, embedded finance, and digital assets.

More infoWeb Summit Rio 2026

Date: June 8–11, 2026

Location: Rio de Janeiro, Brazil

Description: Part of the Web Summit global series, the event connects startups, investors, and tech leaders across Latin America.

More infoFebraban Tech 2026

Date: June 24–26, 2026

Location: São Paulo, Brazil

Description: One of the main financial technology and innovation events for the banking and financial services sector in Latin America.

More info

This week I essentially read the papers mentioned in the intro section (hyperlinks present on last week’s newsletter)

"AI won't replace humans. But humans who use AI will replace those who don't." Sam Altman

espetacular, mto bom, obg