LatAm Tech Weekly

#243: SPECIAL EDITION - STATE OF VC Q2 2026

Weekly writing about what is happening in LatAm tech. By day, I am part of the corporate development team at Itau Unibanco. By night, I am reading and learning about technology in general (now, with a focus on AI). During the weekends, I’m writing the LatAm Tech Weekly. And obviously, always running!

If you have not subscribed yet, join the 14,700+ weekly readers by subscribing here!

Follow me on LinkedIn , Instagram or X for daily updates!

Opinions expressed here are solely my own and does not represent those of people, institutions, organizations that I may or may not be associated with in any capacity, unless explicitly stated.

Happy Sunday!

Unfortunately, Brazil is out. And, right on cue, social media is once again filling up with leadership lessons, management frameworks and confident post-match analysis from people who apparently became football experts overnight…

Those who know me know that I’m a pragmatic person. So, if you came here expecting a profound life lesson—or a business lesson disguised as a soccer analogy—you may want to think again. It will not come from me.

Sometimes there is no hidden message. Brazil lost. The other team played better. The plan did not work. The execution fell short when it mattered. That is sport—and, frankly, that is life too…

Not every defeat needs to become a case study on leadership, culture or high-performance teams. And not every disappointing result requires a five-slide carousel explaining “what CEOs can learn from Brazil’s elimination.” Sometimes the most pragmatic response is simply to accept what happened and move on.

And yes, I realize that writing a post about not turning everything into a lesson is, in itself, turning the defeat into a lesson.

Consider that this is my contribution to the flood…. ;)

A Q2 2026 wrap-up in tech — and why Latin America is watching a completely different movie

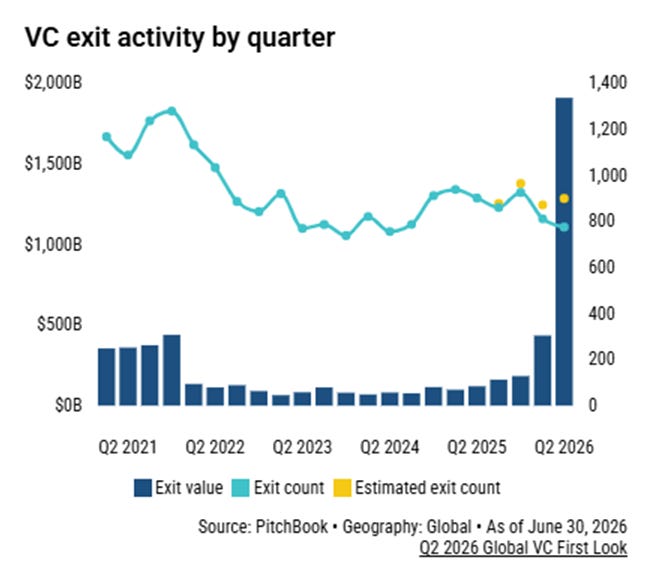

There’s a before and after the day SpaceX went public, and I don’t say that lightly. June’s IPO priced the company at $1.77 trillion — $75 billion raised, the largest public offering in history. On its own, that single deal beat the entire exit value of 2021, which I’ve spent the better part of five years using as *the* reference point for euphoria. It pushed Q2 to nearly $2 trillion in total exit value. SpaceX now sits at a ~$2.1 trillion market cap, the sixth most valuable public company in America. And because apparently one record per company wasn’t enough, less than a week after listing, SpaceX bought Anysphere — the company behind Cursor — for $60 billion. Largest startup acquisition ever.

Think about it: one quarter, two all-time records by one company. And with that, we will obviously talk about concentration... again.

If you’ve been reading this newsletter, you already know where this is going — I’ve written some version of “the AI boom keeps eating the entire market” in basically every issue since Anthropic’s Series H, and I keep expecting the number to plateau, and it keeps not plateauing…

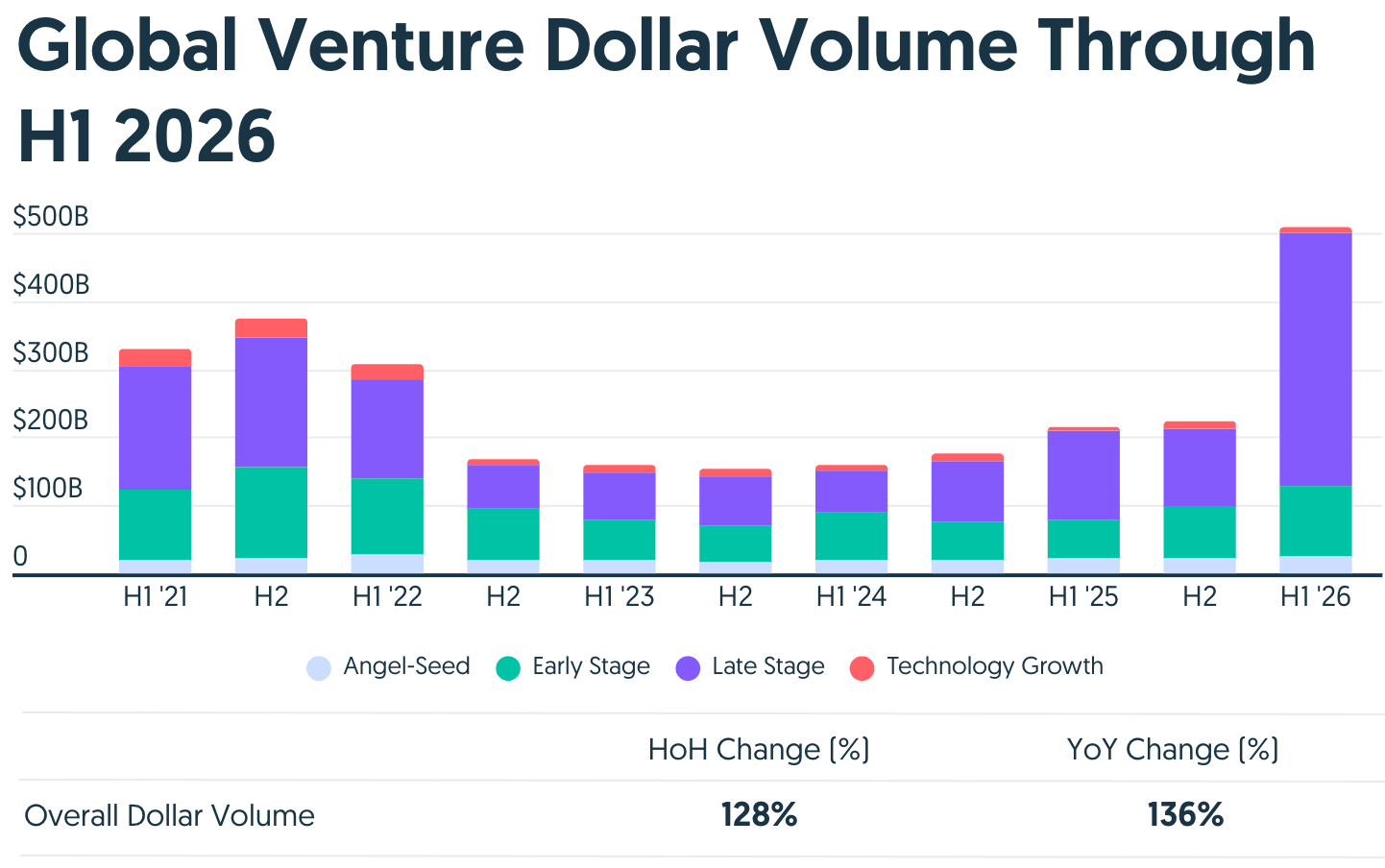

Global venture funding hit $510 billion in H1 2026, per Crunchbase — more than *all of 2025 combined* ($440B), and about 36% above the previous half-year record set back in H2 2021. Q2 alone brought in just over $200 billion, the second-biggest quarter ever, behind only Q1 of this same year. So yes, we’re now comparing quarters to quarters like they’re separate eras.

However, these are the data points that really matter from my point of view (and it’s not the headline figures mentioned above):

- OpenAI and Anthropic raised a combined $217 billion in H1. That’s *43% of every venture dollar deployed globally*, going to two companies. Only two.

- AI captured over 70% of all global funding in Q2 — up from roughly 50% a year ago.

- And yet, AI funding was actually *down* 41% quarter over quarter, to $147 billion, because Q1 had OpenAI’s $122 billion round and there was simply no topping that. Q2’s version was Anthropic’s mega-round, somewhere around $65 billion, pushing it toward a $1 trillion valuation. So “AI funding cooled off” now means it merely dropped to $147B in three months…

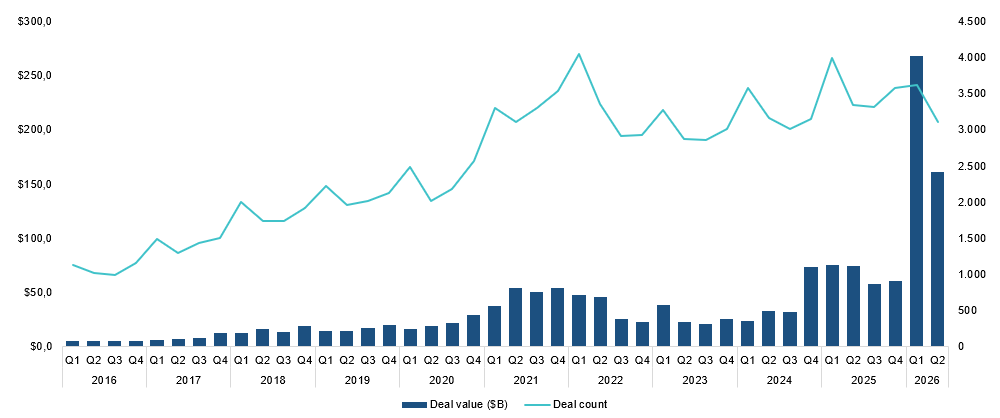

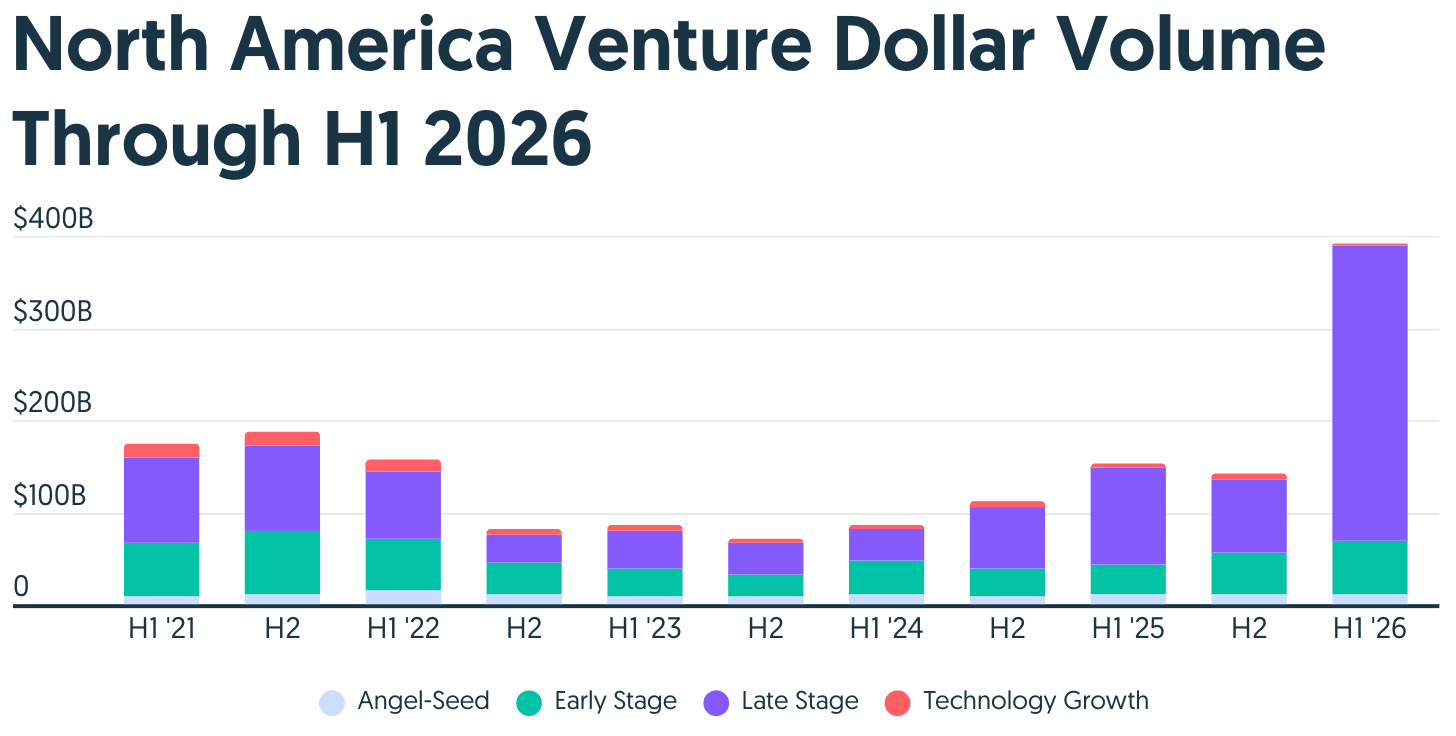

North America told the same story: $392 billion for the half, $137.2 billion in Q2 (+114% YoY) — and deal count fell 26%, to 2,366 rounds. More capital than any point in history, chasing fewer companies than any point in recent memory. Global seed funding for the entire quarter was $12 billion. One frontier-lab round now dwarfs an entire funding stage...

Liquidity actually showed up

For years the standard line at every conference panel I went was “the exit market is broken, nobody can get liquid.” Q2 finally broke that narrative — genuinely the strongest liquidity quarter since 2021, and by dollar value, the strongest ever recorded:

- 32 venture-backed IPOs priced above $1 billion, with Cerebras ($5.6B raised in May) and Quantinuum trailing SpaceX at a very respectful distance.

- 24 acquisitions at $1B+, totaling $113 billion — a record quarter for M&A.

- And a backlog carrying more potential value than the pipeline has ever held, now that OpenAI and Anthropic have both taken their first real steps toward eventual listings.

So yes, the first half of 2026 was record-breaking for venture capital, but the benefits were highly concentrated, leaving smaller and emerging fund managers under increasing pressure. Despite headline exit value reaching $2.19 trillion, much of it came from only a handful of companies, meaning most LPs still received limited distributions and became more selective with new commitments. As a result, capital increasingly flowed to established firms with proven track records: experienced managers captured a record 89% of all VC fundraising and represented 62.2% of funds closed, while billion-dollar funds had an especially strong year. The liquidity squeeze is therefore reinforcing the position of incumbents and making it harder for newer managers—many of whom fund pre-seed and seed startups—to raise capital, although first-time managers with strong prior investing or operating experience remain better positioned.

The trillion-dollar question — and I mean that literally, not as a figure of speech — is whether this liquidity actually reaches LPs broadly, or whether it stays parked in the handful of funds that got an allocation to these three names early. My honest read: it’s going to look exactly like the funding side did. Concentrated. If your fund isn’t in the cap table of one of these three companies, this “best liquidity quarter in five years” should barely touch your DPI. That’s the quiet part nobody wants to say out loud on a panel. Again, the story of concentration...

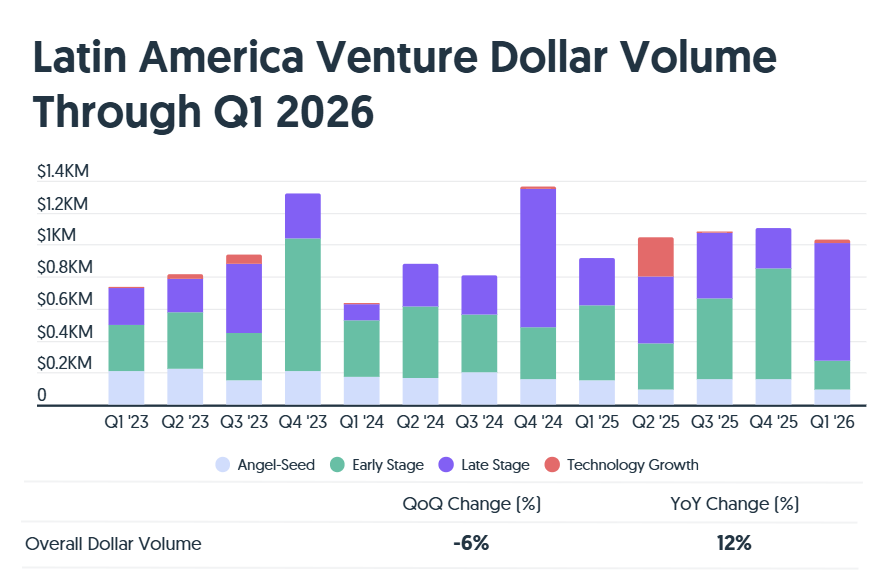

The LatAm double click

While Silicon Valley is burning nine figures on compute in a single afternoon, Latin America is playing an entirely different sport. Regional Q2 reports are still trickling in—Sling Hub and other local trackers typically finalize the numbers over the coming weeks—but the broader picture for the first half of 2026 is already clear: fewer rounds, larger checks, and a level of capital concentration that looks almost modest compared to what's happening in the U.S.

Crunchbase estimates Latin American startups raised $1.03 billion in Q1 2026, up 12% year over year, driven almost entirely by late-stage financings. Growth-stage funding reached $761 million, up 158% YoY, and nearly one-third of all capital deployed during the quarter went to a single company: Kavak's $300 million Series F, led by Andreessen Horowitz and WCM Investment Management. Concentration exists here too—it just happens two orders of magnitude below the OpenAI/Anthropic scale.

A few things worth flagging that explain a lot of what I’m seeing in deal conversations right now:

**Fewer startups are getting funded—but the winners are raising larger rounds. The trend that defined 2025 has continued into 2026. Seed and early-stage deal counts remain subdued, while late-stage financings account for the overwhelming majority of dollars invested. Investors are writing larger checks—but to a much smaller group of companies. That concentration feels remarkably similar to what we're seeing globally, just at a different scale.

**Mexico actually out-raised Brazil in Q1, raising $404 million versus Brazil's $240 million, largely thanks to Kavak's mega-round. It also happened once before—in Q2 2025—but historically Brazil has dominated regional venture funding. The fact that Mexico has now overtaken Brazil twice in the past year suggests this is becoming more than a one-off event.

**A lot of what gets called "venture funding" isn't actually equity. In Brazil, only about 39% of the capital announced in 2025 represented traditional equity financings. The rest came through FIDCs, structured debt and hybrid vehicles. It's a nuance that gets lost every time someone cites a Brazilian "mega-round." A meaningful portion of that capital is financing loan books—not buying ownership in the company. That distinction matters far more than most international datasets acknowledge.

**Exits improved as well. Venture-backed liquidity reached $4.9 billion in 2025, up 172% year over year, while PicPay became the first Brazilian technology company to return to Nasdaq in almost four years. The valuation was noticeably more conservative than peak-cycle expectations—a sign that public markets are rewarding profitability and predictability again, not just growth.

**And yes, AI is here — just not the frontier-lab version. Enter, the São Paulo lawtech founded by ex-Wildlife executives, became the region’s first AI unicorn. Distrito’s Corrida dos Unicórnios 2026 shows all 12 of the region’s top unicorn candidates already use AI somewhere in the business — but only three are AI-first. Around here, AI shows up as margin, not as a model release. It’s automation layered onto fintech, logistics, and services that already worked. Latin America isn't building frontier models. It's building businesses that use AI to improve economics. Less glamorous - probably more durable... It’s a much less exciting story to tell at a conference, and probably a much better one to actually invest behind.

My view

Q2 2026 confirmed something I’ve been circling for a while: there are now two venture markets. One is the frontier AI market, concentrated almost entirely between San Francisco and Seattle, where a handful of companies absorb unprecedented amounts of capital. The other is the rest of venture—Latin America included—where investors are back, but with far higher expectations around efficiency, governance and capital discipline.

I genuinely don’t know which version ages better over the next five years — ask me again after the OpenAI/Anthropic listings actually happen. But I know which one I can put my hands on and make sense of. And for founders in this region, the message from this quarter is not subtle: The capital is back. The tolerance isn’t. Investors aren’t paying for potential anymore—they’re paying for evidence. Traction, efficiency and a differentiated story are no longer competitive advantages. They’re simply the minimum price of admission.

General news:

• A new innovation hub will connect Santa Rita do Sapucaí’s “Electronics Valley” to Brazil’s national startup ecosystem, expanding access to investors, corporations and funding opportunities for deeptech startups. The initiative aims to accelerate commercialization and strengthen Minas Gerais as a leading technology hub. 🇧🇷

Deals:

• Even Realities raised US$150 million in a funding round backed by Meituan, Tencent, Hillhouse Investment and HongShan. Founded by former Apple executive Will Wang, the AI smart glasses startup will use the capital to accelerate product development, expand globally and scale manufacturing, reinforcing investor confidence in AI hardware. 🇨🇳

• B Venture Capital closed its third fund at US$7 million to invest in 20–22 early-stage B2B startups across Latin America. The fund will prioritize AI-native companies and businesses embedding AI agents across sectors such as fintech, SaaS, legaltech, logistics and healthtech. 🌎

General news:

• MSW Capital and Impa Tech partnered to connect mathematics students with venture-backed startups, creating a talent pipeline for AI, data science and deeptech. The initiative aims to bridge academia and startups through real-world projects and future internship programs. 🇧🇷

Deals:

• Mercado Bitcoin raised R$100 million in the first close of its Series C, led by Tether, with SoftBank expected to join the round. The funding will accelerate tokenized assets, on-chain capital markets, crypto lending, payments infrastructure and regional expansion across Latin America. 🇧🇷

• Brazilian fintech Kolek was acquired by RecebeAqui in a share-swap deal that creates a new holding company focused on consolidating vertical fintechs. The combined business aims to triple monthly payment volume by 2027 while expanding its payments infrastructure and improving regulatory efficiency. 🇧🇷

• Mexican fintech Aviva raised a US$18 million Series A led by Valor Capital Group to expand its AI-powered lending platform. The company plans to grow from more than 300 to 1,000 locations while broadening its financial products for underserved consumers. 🇲🇽

• Branddu AI raised a US$300,000 pre-seed round following the merger of Colombia’s Branddu and Mexico’s Reno. The company is building Latin America’s first MerchTech platform to modernize promotional product sourcing through AI and a regional supplier network. 🌎

General news:

• ClickHouse is accelerating its expansion across Latin America, targeting 4–5x regional growth in 2026 as enterprise AI adoption boosts demand for real-time analytics. Following its US$400 million Series D, the company is investing in local teams and AI-native infrastructure, serving customers including OpenAI, Anthropic, Mercado Libre and iFood. 🌎

• Banco do Brasil partnered with the University of Brasília (UnB) to jointly develop AI, data science, cybersecurity and digital innovation projects. The initiative reinforces the banking sector’s growing collaboration with academia to accelerate AI adoption and talent development. 🇧🇷

• Brazil’s split payment model could process 1.3 billion transactions annually starting in 2027 as part of the country’s tax reform. The rollout will initially cover Pix, bank transfers and bank slips, requiring banks and fintechs to adapt their payment infrastructure. 🇧🇷

• Adianta Jus entered the Correios court claims market, providing upfront liquidity to creditors waiting for government-backed receivables. The fintech expects to quadruple revenue in 2026 as it expands into new judicial credit markets. 🇧🇷

• J.P. Morgan launched a dedicated investment banking team focused on companies valued between US$100 million and US$500 million. The initiative expands the bank’s middle-market M&A strategy by targeting succession planning, private equity transactions and capital raising. 🇺🇸

Deals:

• QI Tech acquired Autobanking, expanding into Brazil’s R$280 billion vehicle financing market. The acquisition strengthens its lending-as-a-service platform, with the company aiming to increase Autobanking’s annual revenue from R$50 million to R$300 million within a year. 🇧🇷

• Brendi raised US$6.6 million from Propel Ventures, Big Bets, Norte Ventures and Citrino to expand its AI-powered WhatsApp ordering platform for restaurants. The startup already serves 7,100 restaurants across 1,300 Brazilian cities and is targeting US$20 million in ARR by 2027. 🇧🇷

General news:

• Itaú Unibanco secured its first granted AI patent in Brazil, covering a tool that detects bias in conversational AI responses. The bank is the only financial institution among Brazil’s top five private patent applicants, reinforcing its focus on proprietary AI innovation, responsible AI and model governance. 🇧🇷

• Global venture capital investment reached a record US$412.7 billion in the first half of 2026, surpassing any previous full-year total. AI startups captured 61% of all VC funding, with mega-rounds accounting for more than 80% of invested capital, highlighting the continued concentration of capital around AI infrastructure and enterprise applications. 🌎

• ABSeed Ventures launched ABSeed Winners, a R$100 million evergreen fund focused on follow-on investments and Series B/C startups. The vehicle expands the firm’s strategy beyond B2B SaaS into sectors including AI, healthcare and hardware while providing long-term capital flexibility. 🇧🇷

• Digital bank Plata received regulatory approval to enter Colombia, marking the first step in its regional expansion. Backed by US$2 billion in funding capacity, the fintech plans to launch its digital banking ecosystem in the country in the coming weeks. 🇨🇴

• Fintual is preparing a potential entry into Chile’s pension market after creating a pension services subsidiary and approving an US$8.6 million capital increase. The initiative could expand the wealthtech’s offering beyond investments into fully digital pension management. 🇨🇱

Deals:

• Conta Cheia raised R$50 million to accelerate the growth of its private payroll lending platform. The funding will support technology development, operational scaling and partnerships with medium and large employers as the fintech expands its credit business. 🇧🇷

• Infinia raised US$13.5 million in a Series A led by Bain Capital and Variant Fund to expand its payment infrastructure across Latin America, Africa and Asia. The company connects traditional payment rails with blockchain networks to enable compliant, real-time cross-border settlements. 🌎

• Mexican fintech Digitt secured a US$50 million credit facility from Victory Park Capital to expand its credit card refinancing platform. The funding will grow its loan portfolio and broaden access to lower-cost consumer credit. 🇲🇽

• A consortium led by B Capital Group agreed to acquire Russell Investments for US$2.8 billion. The transaction aims to strengthen the asset manager’s AI capabilities and accelerate innovation across investment management and wealth advisory. 🇺🇸

General news:

• OpenAI launched ChatGPT Work, a new enterprise AI agent that connects to corporate data to automate spreadsheets, presentations, financial forecasting and research. The company also unveiled a desktop AI superapp integrating ChatGPT, Codex and ChatGPT Work, reinforcing its push to become the primary AI productivity platform for enterprises. 🇺🇸

• OpenAI and Google are providing AI models to Chinese groups through Singapore-based subsidiaries, including entities affiliated with Alibaba, Baidu and Tencent that appear on U.S. restricted lists. The practice has intensified debate in Washington over tighter export controls for frontier AI models. 🌎

• Djassi Africa is expanding into Brazil with a strategy focused on supporting underrepresented founders through capital, mentorship and international networks. The initiative strengthens connections between African and Latin American startup ecosystems. 🇧🇷

Deals:

• Núclea agreed to acquire Data Rudder, expanding its fraud prevention, AML and transaction monitoring capabilities. The companies expect the integration to significantly improve disputed-fund recovery rates across Brazil’s financial ecosystem. 🇧🇷

• Chilean AI startup Lilo was acquired by U.S.-based Inn-Flow less than three years after its founding. The acquisition strengthens Inn-Flow’s hospitality platform while validating Latin America’s ability to build globally competitive enterprise AI companies. 🇨🇱

• Serasa Experian plans to continue its M&A strategy after investing nearly R$2.5 billion across 17 acquisitions since 2020. The company is evaluating targets in fraud prevention, credit risk, healthcare and data services while complementing acquisitions with a corporate venture capital program. 🇧🇷

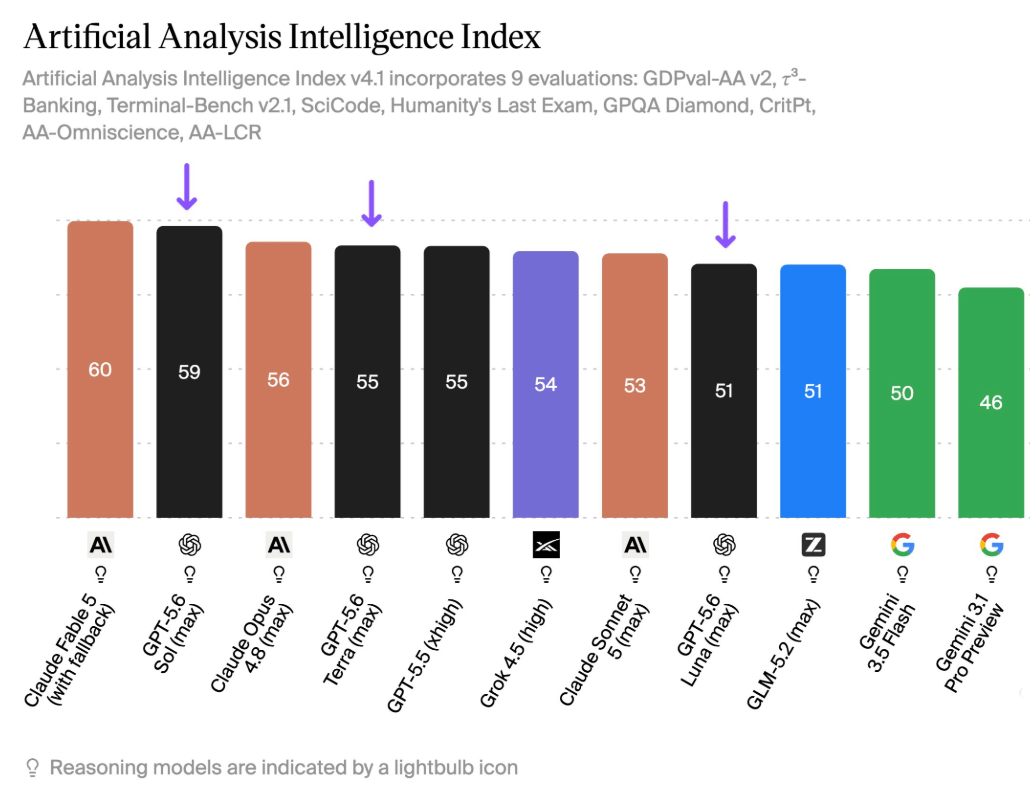

The biggest AI story of the week came on July 9, when OpenAI broadly released GPT-5.6 and introduced a three-model lineup led by its new flagship, Sol. Predictably, X quickly filled with benchmark charts, pricing comparisons and people declaring a new winner in the model race. Much of the excitement centered on efficiency: Artificial Analysis ranked Sol just behind Anthropic’s Claude Fable 5 while estimating that it delivers similar intelligence at roughly one-third of the cost, with particularly strong results in coding and presentation-style work. The reaction was not universally celebratory, however, as some users pointed to only modest gains over GPT-5.5 in certain tests and a higher measured hallucination rate. My takeaway is that GPT-5.6 may not represent a dramatic new leap in raw intelligence, but it reinforces what increasingly matters in this market: how much useful work a model can complete for each dollar spent.

Febraban Tech 2026

Date: August 24–26, 2026

Location: São Paulo, Brazil

Description: One of the main financial technology and innovation events for the banking and financial services sector in Latin America.

More infoConta Azul Con 2026

Date: August 1, 2026

Location: São Paulo, Brazil

Description: A conference connecting accounting, entrepreneurship, and technology through keynotes, workshops, networking sessions, and discussions on business innovation.

More infoRio Innovation Week 2026

Date: August 4–7, 2026

Location: Rio de Janeiro, Brazil

Description: One of Brazil’s largest innovation festivals, bringing together entrepreneurs, startups, corporations, investors, and policymakers to discuss technology, business, and social transformation.

More infoSP2B (São Paulo Beyond Business) 2026

Date: August 9–16, 2026

Location: São Paulo, Brazil

Description: A new business and innovation event designed to connect entrepreneurs, executives, investors, and corporations through discussions on growth, creativity, and the future of business.

More infoDeep Tech Summit 2026

Date: August 11–12, 2026

Location: São Paulo, Brazil

Description: A conference focused on science-based innovation, bringing together deep tech startups, investors, corporations, and researchers to explore frontier technologies and emerging opportunities.

More infoStartup Summit 2026

Date: August 26–28, 2026

Location: Florianópolis, Brazil

Description: One of Latin America’s leading startup events, connecting founders, investors, and ecosystem leaders through content, networking, and business opportunities.

More infoHackTown 2026

Date: September 3–7, 2026

Location: Santa Rita do Sapucaí, Brazil

Description: A unique innovation, technology, and culture festival that transforms an entire city into a hub for networking, learning, entrepreneurship, and creative collaboration.

More infoHotmart Fire 2026

Date: September 10–12, 2026

Location: Belo Horizonte, Brazil

Description: One of the leading events for the digital business and creator economy ecosystem, covering marketing, sales, online education, innovation, and business growth.

More infoDreamforce 2026

Date: September 15–17, 2026

Location: San Francisco, United States

Description: Salesforce’s flagship conference focused on CRM, AI, digital transformation, customer experience, and enterprise innovation.

More infoTechCrunch Disrupt 2026

Date: October 13–15, 2026

Location: San Francisco, United States

Description: A leading global startup conference where founders, investors, and technology leaders discuss entrepreneurship, fundraising, and innovation.

More infoWeb Summit Lisbon 2026

Date: November 9–12, 2026

Location: Lisbon, Portugal

Description: One of the world’s largest technology conferences, bringing together entrepreneurs, investors, executives, and policymakers to discuss global innovation trends.

More infoSlush 2026

Date: November 18–19, 2026

Location: Helsinki, Finland

Description: A globally recognized startup and venture capital conference focused on connecting founders and investors while fostering innovation and growth.

More infoAWS re:Invent 2026

Date: November 30 – December 4, 2026

Location: Las Vegas, United States

Description: AWS’s flagship cloud computing conference, featuring product launches, technical sessions, training, and discussions on cloud infrastructure, AI, and data.

More info

Crunchbase - Global Startup Investment Hit Record $510B In H1 2026 As AI Boom Accelerates Funding And Exits

“Sempre procurei jogar com um sorriso no rosto.”

— Ronaldinho Gaúcho

“I have always tried to play with a smile on my face.”

— Ronaldinho Gaúcho