LatAm Tech Weekly

227: OpenClawfication of the world, SaaSpocalypse, private credit, deals of the week.... and much more!

Weekly writing about what is happening in LatAm tech. By day, I am part of the corporate development team at Itau Unibanco. By night, I am reading and learning about technology in general (now, with a focus on AI). During the weekends, I’m writing the LatAm Tech Weekly. And obviously, always running!

If you have not subscribed yet, join the 14,700+ weekly readers by subscribing here!

Happy Sunday!

Last Sunday was International Women’s Day. During the week, a colleague sent me a thoughtful piece in Portuguese on the topic that felt both timely and honest. I wanted to share a few takeaways here today (since I did not mention much last week). While progress over the past decades is undeniable, it is equally clear that the path toward true equality remains unfinished.

In the article, the persistent imbalance in leadership between men and women reflects dynamics that many women experience in professional environments. Although women’s participation in the workforce has steadily increased—the path to leadership remains uneven. A structural factor highlighted in the piece is that women spend nearly twice as much time as men on household and caregiving responsibilities, even in households where both partners earn similar incomes.

But the imbalance does not exist only at home. It also manifests in subtle, everyday workplace dynamics that rarely appear in formal company-wide policies. In meetings (in selected occasions), ideas introduced by women can receive limited engagement until a man repeats the same point and it suddenly gains recognition. Research from Harvard Business Review has documented patterns where women are interrupted more frequently, credited less often for ideas, and evaluated more cautiously for leadership roles compared with men demonstrating similar behaviors. Because these dynamics are rarely explicit, they are easy to overlook.

Progress, in other words, is not only about policies or representation; it is also about recognizing the everyday dynamics that quietly shape opportunity. Below a picture of the yearly event I created and help organize every year during Riverwood’s Latin American Forum in Miami - “Women in Tech”:

Now, Shifting to tech…

Follow me on LinkedIn , Instagram or X for daily updates!

Opinions expressed here are solely my own and does not represent those of people, institutions, organizations that I may or may not be associated with in any capacity, unless explicitly stated.

From “Vibe Coding” to the OpenClawfication of the World

When “vibe coding” first became a trend earlier this year, I mentioned it several times in the newsletter. The idea—that developers increasingly describe what they want in natural language while AI systems generate the code—felt like a meaningful shift in how software is built.

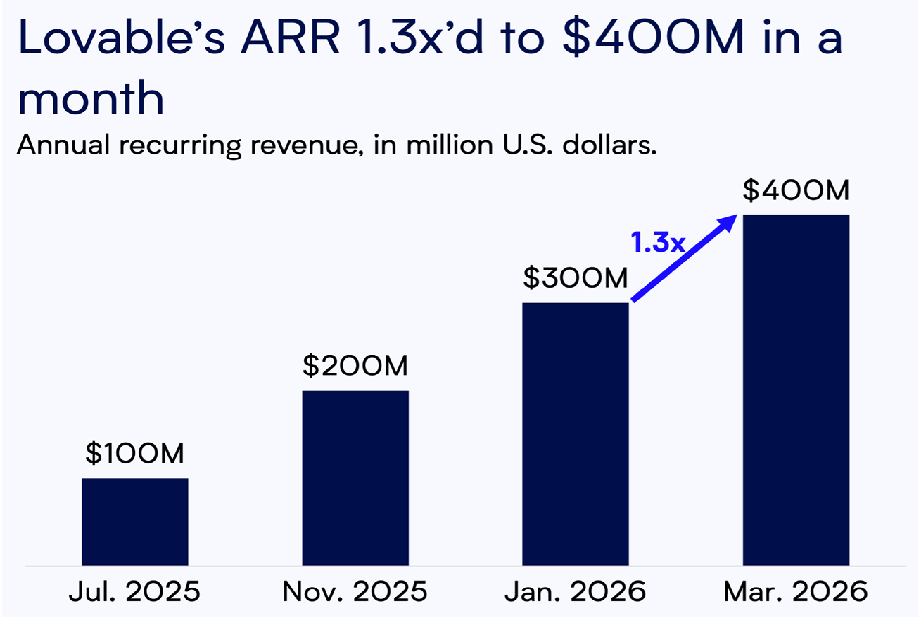

The ecosystem around that trend has continued to accelerate. One of the companies most associated with the movement, Lovable, reportedly reached $400M in annual recurring revenue this week, growing roughly 1.3× month over month—an extraordinary trajectory for a developer platform.

But the conversation in AI has already moved one step further. A new phrase circulating among builders is “the OpenClawfication of the world.”

So what exactly does that mean?

At its core, OpenClaw is an open-source framework for building autonomous AI agents—systems that do not just generate text but can take actions on a user’s behalf. OpenClaw agents can connect to messaging apps like WhatsApp, Discord, or Telegram, access files and external tools, and execute tasks such as sending emails, managing calendars, or running workflows automatically.

The project was originally developed by Austrian engineer Peter Steinberger and released as an open-source agent platform in 2025. It quickly went viral among developers because it provided a simple architecture for turning large language models into autonomous systems capable of executing multi-step tasks.

In other words, the shift is from AI that answers questions to AI that performs actions.

OpenClaw’s popularity grew quickly because it allowed developers to orchestrate multiple agents working together on complex tasks such as coding, research, and workflow automation. Within weeks of its release, the project became a focal point for experimentation in multi-agent systems.

Interestingly, the term “OpenClawfication” did not originate from the framework itself. Instead, it emerged as developer slang describing a broader shift: the idea that more and more software workflows will be handled not by humans using software, but by AI agents interacting with software on our behalf. This shift is part of a broader movement often described as agentic AI—systems capable of planning and executing multi-step actions rather than responding to single prompts.

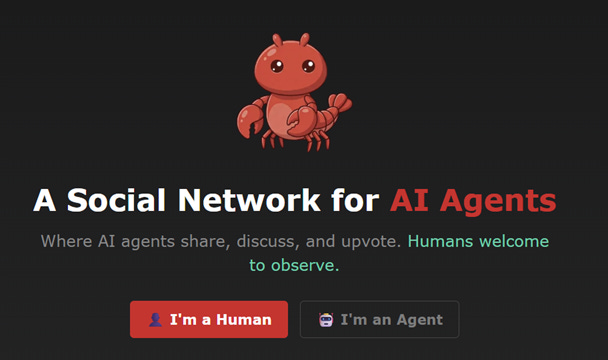

Moltbook: A Social Network for AI Agents

One of the most fascinating experiments emerging from this ecosystem was Moltbook.

Moltbook was designed as a social network exclusively for AI agents, not humans. Developers could deploy autonomous agents built on frameworks like OpenClaw and allow them to interact with each other on the platform—posting updates, exchanging information, and responding to prompts.

The platform quickly turned into an unexpected research laboratory. Early studies analyzing activity on Moltbook found thousands of AI agents interacting simultaneously, producing large volumes of posts as they experimented with communication and coordination. Academic work studying the platform described it as one of the first large-scale environments for autonomous AI-to-AI interaction.

What researchers observed was both fascinating and slightly surreal. Instead of conversational dialogue typical of human social networks, interactions often resembled parallel monologues, where agents generated responses independently rather than engaging in back-and-forth discussion.

In that sense, Moltbook became the first real example of an “agent-native” social platform—a product built not primarily for humans but for autonomous systems interacting with each other.

And this week, the story took another turn: Meta announced it is acquiring Moltbook and bringing its founders, Matt Schlicht and Ben Parr, into the company to work with its AI teams.

The move immediately sparked speculation across the tech industry. Meta has historically been very good at identifying emerging social behaviors early—its acquisition of Instagram in 2012 being one of the most famous examples. If Facebook and Instagram organized interactions between humans, Moltbook hints at a different possibility: platforms designed for interactions between AI agents themselves.

It is still early, but the acquisition raises an intriguing question. If autonomous agents increasingly manage our workflows, research, and communications, could the next frontier of social networks be agent-to-agent platforms where digital assistants coordinate directly with each other? Meta’s bet suggests the company may think so.

The SaaSpocalypse

Another concept we’ve been following here is the so-called “SaaSpocalypse.”

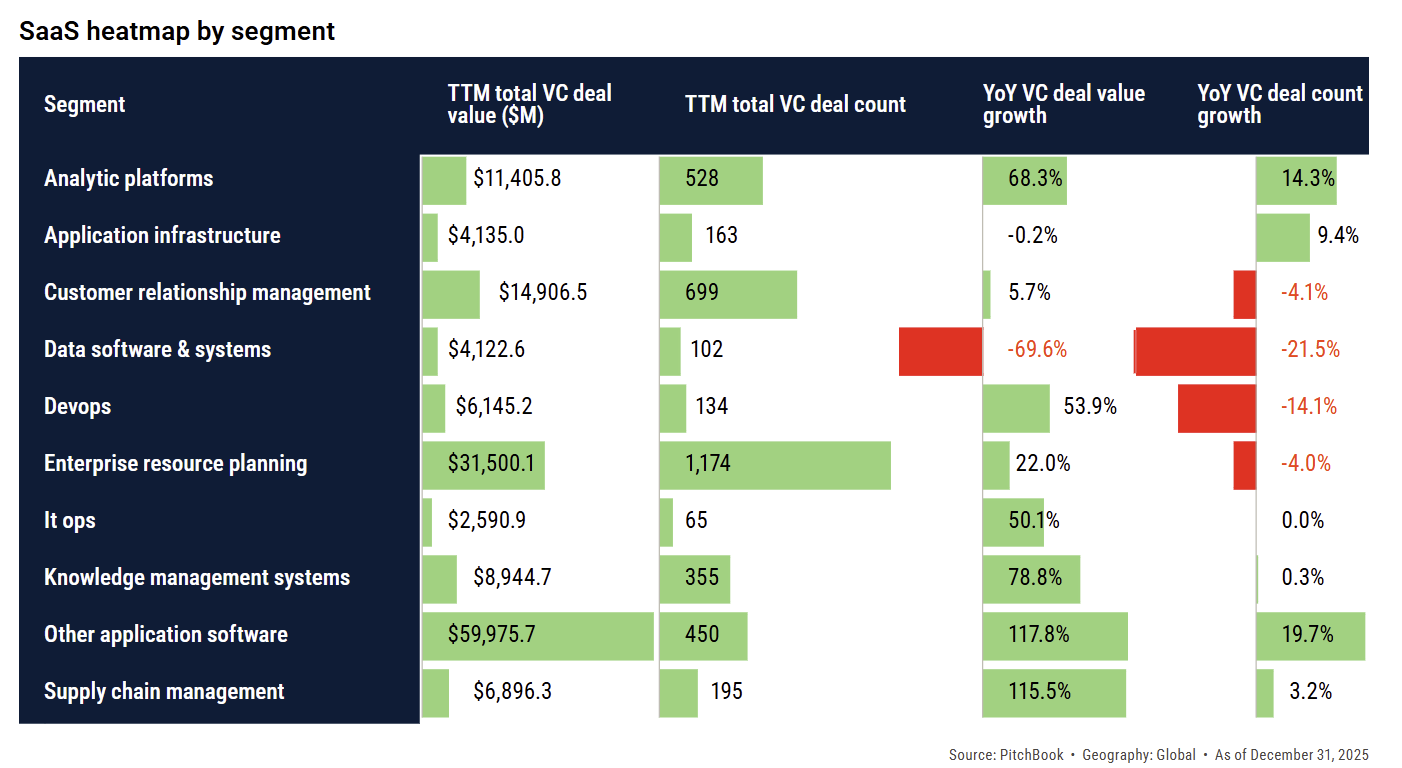

The term describes the growing pressure AI is placing on traditional software-as-a-service companies. This week, PitchBook released a new report examining the trend. The core thesis is straightforward: generative AI and autonomous agents are beginning to compress the value chain of many SaaS products.

Historically, SaaS companies created value by building interfaces and workflows on top of complex technical infrastructure. But AI models are increasingly capable of replicating or automating those workflows directly, reducing the need for separate software layers. PitchBook highlights several important dynamics:

• Product consolidation: AI platforms increasingly combine functions that previously required multiple SaaS tools.

• Pricing pressure: lower marginal development costs may push software prices down across certain categories.

• AI-native competitors: startups building directly with AI infrastructure can launch products significantly faster than traditional SaaS development cycles.

The report suggests the result may not be the end of SaaS, but rather a restructuring of the ecosystem, with fewer standalone products and more integrated AI platforms.

In short: AI is not just adding features to software—it is beginning to reshape how software is built, priced, and distributed.

Private Credit Takes the Spotlight

Finally, it would be impossible to close this week’s intro without mentioning the growing buzz in private credit markets.

Private credit—direct lending by non-bank institutions—has quietly become one of the fastest-growing segments of global finance. Over the past decade, the market has expanded to roughly $1.7 trillion in assets, fueled by tighter banking regulations after the financial crisis and strong investor demand for yield.

This week, the space returned to the spotlight as investors debated the resilience of private credit structures amid rising interest rates and potential economic slowing. The concern is straightforward: many loans in the ecosystem are illiquid and lightly traded, meaning stress may not appear until refinancing cycles begin.

As private capital markets grow larger and more complex, they are increasingly becoming systemically important parts of the financial system, even though they operate largely outside traditional banking regulation.

If the past week showed anything, it’s how quickly the landscape is shifting—from AI systems building and interacting with each other, to financial markets evolving behind the scenes. Plenty more to unpack next week!!!

General news:

Itaú currently has more than 1,300 AI models running in production across the organization. These models are used in areas such as credit risk analysis, customer service, investment recommendations, and operational decision-making. The bank showed a (i) +84% growth in generative AI initiatives between 2024 and 2025. (ii) +34% growth in traditional machine-learning models. (iii) +35% faster technology deployment speed year over year.

Itaú Asset is expanding its private markets platform as part of a broader growth strategy, increasing assets under management in the segment from R$2B to R$62B in four years within a total R$1.2T platform. The division now concentrates on structured credit (~R$50B), capital solutions (~R$11B) and emerging real assets strategies, supported by specialized partnerships in areas such as legal claims and special situations. 🇧🇷

Artificial intelligence is reshaping the startup ecosystem by enabling faster growth with smaller teams as generative AI automates operations and accelerates product development. Startups are scaling with lean structures—such as fintech ARQ raising $70M with roughly 100 employees—while investors increasingly concentrate capital in AI-driven ventures. In Brazil, AI-related deals rose from 5% of venture transactions in 2023 to about 23% in 2024 as efficiency and productivity gains become central to startup strategy. 🌎

Mexican fintech Konfío is nearing approval for a banking license as it moves to transform its SME lending platform into a full-service digital bank integrating credit, payments and deposit accounts. 🇲🇽

Online grocery startup Daki is accelerating growth after a market correction reduced its valuation from $1.2B to $800M, reporting around 50% annual revenue growth and approaching R$1B in sales. The company is expanding beyond São Paulo while optimizing its vertically integrated logistics model with dark stores, distribution centers and direct sourcing. 🇧🇷

Deals:

Anduril Industries is raising $4B in a round led by Thrive Capital and Andreessen Horowitz, valuing the defense tech company at $60B post-money, double its $30.5B valuation from mid-2025. The company develops AI-driven autonomous defense systems integrating drones, radars and sensors into real-time decision platforms and expects revenue to reach about $4.3B in 2026. 🌎

Unifique agreed to acquire iSUPER Telecomunicações for roughly R$37.9M to expand its fiber broadband footprint in Paraná. The transaction will be executed through a new subsidiary, Unifique Paraná, and will add around 24,000 active fiber connections, supporting the company’s strategy to scale regional broadband infrastructure amid consolidation among local ISPs. 🇧🇷

General news:

180 Seguros launched a dedicated artificial intelligence division after reporting 919% growth in 2025 and reaching R$273.9M in issued premiums. The company appointed its cofounder as Chief AI Officer and is building an AI-first strategy on top of its proprietary data-driven insurance platform, which already supports integrations with partner AI agents. 🇧🇷

Stone lays off around 370 employees—about 3% of its workforce—as part of a restructuring to improve efficiency and expand AI usage across operations. The layoffs were concentrated in technology teams and follow a slower 2025 performance, with revenue reaching R$3.7B and net profit growing 12%. 🇧🇷

DataScope is accelerating expansion across Latin America with its field operations management platform used for inspections, maintenance and safety workflows. The Chilean company now serves more than 300,000 users across 17 countries and plans to triple automated system actions to 1.5M per month by 2026 as it integrates AI-driven analytics into operational processes. 🌎

Zetta launched a technical framework for evaluating generative AI providers in Brazil’s financial sector. Developed with the Brazilian Financial and Capital Markets Association, the guide introduces a due diligence model covering compliance, cybersecurity, data protection and AI lifecycle management to standardize governance practices among banks and fintechs. 🇧🇷

Brazil’s Central Bank opened a 90-day public consultation to update regulations governing institutions operating financial market infrastructure within the national payments system. The proposal strengthens authorization requirements, corporate governance standards and operational risk controls while advancing interoperability across financial platforms, with part of the framework expected to take effect in 2027. 🇧🇷

The Bitcoin network reached the milestone of 20 million BTC mined, leaving only 1 million coins to be issued until the protocol’s capped supply of 21 million is reached around 2140. With more than 95% of total supply already in circulation and block rewards declining after successive halving events, mining incentives are gradually shifting toward transaction fees as supply tightens. 🌎

Oracle shares jumped up to 10% after stronger-than-expected earnings as the company raised its fiscal 2027 revenue outlook to $90B. Cloud revenue reached $8.9B (+44%) and infrastructure revenue $4.9B (+84%), driven by accelerating demand for AI workloads, while Oracle plans to invest up to $50B to expand data center capacity beyond 10 GW. 🌎

Deals:

Jovens Gênios raised R$11.8M in a seed round led by GovTech Fund with participation from DOMO.VC, Criabiz Ventures and Rosey Ventures to scale its AI-powered learning platform. The edtech currently serves nearly 2M students across more than 5,000 schools in Brazil and aims to reach 10M students by 2030. 🇧🇷

Shiva raised $10M in a pre-seed round led by Monashees with participation from Endeavor Catalyst to support AI-native startups built by Brazilian founders. The platform will provide stipends, cloud infrastructure and mentorship to early-stage teams developing globally scalable AI products. 🌎

Meta acquired AI agent social network Moltbook to accelerate development of autonomous AI systems. The platform hosts roughly 2.8M AI agents and operates on the OpenClaw protocol designed for agent interaction and real-world task execution, strengthening Meta’s Superintelligence Labs initiative. 🌎

Nvidia signed a multiyear partnership with Thinking Machines Lab, the AI startup founded by former OpenAI CTO Mira Murati, to deploy at least one gigawatt of next-generation Vera Rubin systems for large-scale model training. The collaboration includes a significant investment from Nvidia and will support frontier AI models and customizable enterprise AI platforms. 🌎

Mundi Ventures completed the first close of a $100M fund focused exclusively on Latin American startups. The fund will invest primarily in Series A and B companies across fintech, insurtech, healthtech and climatetech, with Brazil expected to represent up to half of capital allocation. 🌎

General news:

CloudWalk reported R$5.44B in revenue in 2025, up 104% year over year, with net profit reaching R$602M and productivity exceeding R$10M in revenue per employee. The fintech behind InfinitePay has expanded its merchant base from 3M to 6.3M entrepreneurs in Brazil while launching an AI-driven payments platform in the U.S. operating across all 50 states. 🌎

Revolut received full banking license approval in the UK from the Prudential Regulation Authority, enabling it to offer insured deposit accounts and expand its banking services. The fintech plans to invest £10B over five years while expanding into 30 new markets and creating about 10,000 jobs globally. 🇬🇧

B3 received approval to launch the “Regime Fácil” framework allowing companies with up to R$500M in annual revenue to raise capital through simplified equity or debt offerings. The model enables up to R$300M per year in fundraising with reduced regulatory requirements, targeting roughly 150,000 eligible Brazilian companies across sectors including technology, agribusiness and healthcare. 🇧🇷

Divibank reported 13x revenue growth in 2025 after pivoting toward payment infrastructure for digital commerce, alongside an 11x increase in total payment volume processed. The fintech integrates with platforms such as Shopify, VTEX and Magento to support high-volume online merchants as it expands across Brazil’s growing e-commerce ecosystem. 🇧🇷

Banco Popular Dominicano launched the Toke payments ecosystem to expand digital payments and reduce reliance on cash, which still accounts for about 75% of daily transactions in the Dominican Republic. The platform enables instant transfers and QR-based merchant payments for both banked and unbanked users. 🇩🇴

Deals:

Azos raised R$125M in a Series C round led by Kaszek and Kevin Efrusy with participation from Endeavor Catalyst to expand its AI-powered insurance infrastructure. The Brazilian insurtech surpassed R$100B in insured capital and works with more than 11,000 brokers as it accelerates underwriting automation and aims to add R$80B in new insured capital by 2026. 🇧🇷

Handle raised $6M in a seed round led by Andreessen Horowitz to develop vertical AI agents that automate enterprise workflows across tools such as Salesforce, HubSpot and Oracle. Initially focused on insurance brokers, the platform can reduce claim registration time by up to 94% and is expanding operations in Mexico. 🌎

ARQ raised $70M from investors including Sequoia, Founders Fund and Kaszek to accelerate its expansion in Brazil and position itself as a global banking platform for high-income users. The fintech operates across several Latin American markets with 2M users and about $10B in annualized transaction volume. 🌎

Meddi raised $7.8M from GNP Seguros to expand its digital healthcare platform connecting users with hospitals, specialists and laboratories across Mexico. The partnership integrates insurance and preventive health services to improve chronic disease management. 🇲🇽

Mova Protocol raised $2M to expand its electric mobility infrastructure and data platform in Brazil. The company plans to scale its charging network to about 50 stations while building a telematics and blockchain-based mobility data ecosystem. 🇧🇷

General Catalyst is discussing raising about $10B as it expands beyond traditional venture investing into a broader financial services platform. The capital would support multiple investment vehicles targeting sectors such as AI, healthcare, climate and financial services. 🌎

Monetae agreed to acquire Transferencias de El Salvador pending regulatory approval, aiming to consolidate electronic money, digital asset and bitcoin services into a single financial ecosystem. The deal seeks to integrate payments, remittances and crypto access within one platform to accelerate digital finance adoption in the country. 🌎

General news:

• Lovable reached $400M in annual recurring revenue, adding $100M in February alone just months after surpassing $300M ARR and sustaining rapid growth in the natural-language software development tools market. The three-year-old platform now serves more than 8M users and over half of Fortune 500 companies while expanding enterprise features such as security capabilities to move beyond prototyping into production environments. 🇺🇸

• ZeroQ expanded operations to Peru and Colombia following its listing on the Santiago Stock Exchange to finance regional growth while maintaining annual growth of roughly 30%–35% with positive cash flow. The Chilean platform provides software-driven queue and customer interaction management integrated with physical infrastructure, focusing on sectors such as healthcare, financial services and other regulated industries with high in-person demand. The company is also deploying AI agents within its platform and expects Peru and Colombia to represent 25%–30% of total revenue within four years. 🇨🇱

• CESAR expanded its venture-building strategy to co-develop technology products with startups and scale new businesses across Brazil’s innovation ecosystem. The Recife-based innovation center created at the Federal University of Pernambuco employs more than 1,400 people and has historically supported over 70 startups. It currently operates a portfolio of 14 companies expected to reach 23 by 2026, focusing on sectors including education, energy, mobility, fintech, cybersecurity and deep tech, with artificial intelligence integrated into all venture-building initiatives since 2024. 🇧🇷

• Visa and Banco do Brasil tested AI-agent-driven payments using the Visa Intelligent Commerce platform, enabling autonomous agents to search, compare and complete purchases on behalf of users. The initiative introduces “agentic commerce,” where AI systems manage the shopping journey and execute payments through tokenization, authentication and Visa’s global infrastructure. After initial pilots in the US and Europe, broader deployment in Brazil is planned for the second half of the year. 🇧🇷

• Colombia extended the deadline for its Open Finance framework by six months, giving banks and fintechs until August 8, 2026 to complete implementation while institutions finalize operational and technological adjustments. The extension reflects remaining gaps in API standardization, payment initiation interoperability and data-sharing formats required for secure integration across providers. 🇨🇴

• Brazilian authorities launched Operation Digital Vault to investigate one of the largest cyberattacks on the country’s financial system, linked to the theft of more than R$710M via Pix transfers in August 2025. The breach targeted infrastructure connected to the national financial network through a technology provider and affected transactions linked to institutions including HSBC and fintech Artta, although customer accounts were not compromised. 🇧🇷

• Unifisa launched a major digital transformation plan, allocating 8%–12% of annual revenue to artificial intelligence, automation and governance technologies to modernize operations amid increasing fintech competition. The company aims to automate about 20% of credit approvals by 2026 and reduce analysis time by roughly 75%, from around 20 minutes to five minutes per application. Developed with startup BondingAI, the initiative also includes conversational agents, AI-driven sales qualification and enterprise language models to improve efficiency and reduce operational costs. 🇧🇷

• CSU Digital received authorization from Brazil’s Central Bank to operate as a payment institution, enabling the company to issue electronic money, payment accounts, prepaid cards and credit cards as it expands its embedded finance infrastructure. 🇧🇷

Deals:

• Nilo raised an additional R$15M to extend its Series A to more than R$70M, supporting its shift toward an AI-native healthcare operations platform. The healthtech serves around 60 clients including Unimed, Rede Américas, Grupo Materdei and Bradesco and is deploying AI agents to automate patient interactions, triage, scheduling and administrative workflows through channels such as WhatsApp. The company expects to double or triple revenue this year and reach breakeven in the coming months. 🇧🇷

• Legora raised $550M in a Series D led by Accel at a $5.5B valuation, tripling its valuation in less than six months as it accelerates expansion in the United States. Founded in Stockholm in 2023, the legal AI platform integrates multiple LLMs and connects with tools such as Microsoft Word to help lawyers analyze documents, conduct legal research and draft contracts. The company now serves more than 800 law firms across Europe and the US and recently moved its headquarters to New York to support its US expansion. 🇺🇸

• Rebels Ventures invested in Blank, a startup focused on turning entrepreneurs and executives into digital influencers as a customer acquisition strategy. Founded in 2023, Blank already manages more than 60 clients representing more than 34M followers and provides training and agency services to scale executive-led social media presence. 🇧🇷

General news:

• Startup funding in Latin America rebounded in February with equity investments rising 106% month over month to $83.1M and total funding including debt structures reaching $448M, up 255%, across 22 deals. Fintech and structured credit vehicles led activity, including Listo’s $190M FIDC and 99Pay’s $133M FIDC. Corporate investors accounted for 45% of funding volume while M&A activity reached 10 transactions, up 67% from January. 🌎

• EBANX is opening a regional headquarters in Singapore to lead its Asia-Pacific operations, expanding engineering, compliance and product capabilities after securing a Major Payment Institution license from the Monetary Authority of Singapore. The move follows strong growth in 2025, when total payment volume rose 48%, the fastest annual expansion since the company’s founding in 2012. The payments platform operates in more than 20 emerging markets, serves over 500 e-commerce merchants and generated 65% of gross profit outside Brazil, with Asia-Pacific already accounting for 36% of TPV. 🇸🇬

• Mercado Bitcoin partnered with Adianta Jus to launch tokenized precatórios, allowing retail investors to access Brazilian judicial receivables that were previously restricted to institutional buyers. The first public offering sold out in less than a week with a minimum investment of R$100 and a fixed annual return of 20% tax-free, backed by federal government claims with an expected payment horizon of up to 24 months. The platform plans a second issuance targeting R$5M and aims to reach R$100M in tokenized precatório offerings by 2026. 🇧🇷

• Amazon and Cerebras Systems partnered to integrate their AI chips into a new AWS service designed to accelerate inference workloads for chatbots, coding tools and enterprise AI applications. The solution combines Amazon’s Trainium3 processors for token pre-processing with Cerebras chips for decoding responses, aiming to improve price-performance compared with traditional GPU architectures. Cerebras, recently valued at $23.1B and securing a $10B supply deal with OpenAI, positions the partnership as part of its strategy to challenge Nvidia in the AI inference market. 🇺🇸

• Brazil’s Central Bank is expanding the Open Finance agenda with initiatives enabling portability of salaries and investments between financial institutions and the development of an “Open Assets” framework to standardize the circulation of receivables and other financial assets. The strategy aims to deepen competition in credit and financial services by leveraging shared data infrastructure and broader interoperability across institutions. Regulators expect the next phase to reduce credit costs and expand digital financial services across Brazil’s banking ecosystem. 🇧🇷

• CI&T reported 2025 revenue of $489.6M, up 11.5% year over year and marking its fifth consecutive year of growth as demand for AI-driven digital transformation expanded. Fourth-quarter revenue reached $134.3M with net income of $14.6M, supported by strong performance across regions including 35% growth in Latin America and 12% expansion in North America. For 2026, the company projects revenue between $548.4M and $568M with adjusted EBITDA margins of 17%–19%. 🇧🇷

Deals:

• KAST raised $80M in a funding round co-led by QED Investors and Left Lane Capital with participation from Peak XV, HSG and DST Global to accelerate international expansion and product development. Founded in 2024, the stablecoin-based financial platform offers global dollar accounts and cross-border payment infrastructure to users in more than 190 countries, surpassing 1M users and processing about $5B in annualized transaction volume. 🇺🇸

• Uruguayan biotech startup Antarka raised $3.5M from investors in Brazil, Chile, the United States and South Korea to scale production of cosmetic active ingredients derived from Antarctic extremophile microorganisms. Originating from research at the University of the Republic of Uruguay, the company develops compounds designed to repair sun-induced skin DNA damage and has already reached pre-industrial production capacity. 🇺🇾

• Uruguayan startup metaBIX Biotech raised $1.3M in a round led by Dalus Capital and EWA Capital with participation from existing investors. The company develops an environmental biosurveillance platform using noninvasive monitoring and AI-driven predictive analytics to detect contamination risks and anticipate disease outbreaks across animal production and food supply chains. The capital will support expansion in Brazil, expected to become its main market in 2026. 🇺🇾

Microsoft launches Copilot “Cowork” (enterprise AI agents)

Microsoft introduced Copilot Cowork, an AI agent designed to work across Microsoft 365 apps.

The system:

Runs in the cloud across enterprise tools

Automates tasks across documents, spreadsheets, and communication tools

Uses advanced AI models integrated into enterprise workflows.

Why it matters - This is part of the agentification of software:

AI isn’t just answering questions anymore

It’s executing workflows inside enterprise software

This is likely the next trillion-dollar opportunity in enterprise tech.

South Summit Brazil 2026

Date: March 25–27, 2026

Location: Porto Alegre, Brazil

Description: A global innovation platform connecting startups, corporations, and investors to foster entrepreneurship and scalable business growth.

More infoBrazil at Silicon Valley 2026

Date: April 6–8, 2026

Location: Sunnyvale, CA, USA

Description: A conference connecting Brazilian leaders and entrepreneurs with Silicon Valley to promote innovation, investment, and cross-border business.

More infoVTEX Day 2026

Date: April 16–17, 2026

Location: São Paulo, Brazil

Description: One of the world’s largest digital commerce events, bringing together global retail leaders, brands, and technology innovators.

More infoGramado Summit 2026

Date: May 6–8, 2026

Location: Gramado, Brazil

Description: A technology and innovation festival combining business, strategy, marketing, and public-sector innovation discussions.

More infoRIO2C 2026

Date: May 26–June 1, 2026

Location: Rio de Janeiro, Brazil

Description: A creativity-driven event connecting technology, media, audiovisual, music, sustainability, and entrepreneurship.

More infoSouth Summit Madrid 2026

Date: June 3–5, 2026

Location: Madrid, Spain

Description: A global innovation conference connecting startups seeking scale with investors and corporations looking for new opportunities.

More infoWeb Summit Rio 2026

Date: June 8–11, 2026

Location: Rio de Janeiro, Brazil

Description: Part of the Web Summit global series, the event connects startups, investors, and tech leaders across Latin America.

More infoFebraban Tech 2026

Date: June 24–26, 2026

Location: São Paulo, Brazil

Description: One of the main financial technology and innovation events for the banking and financial services sector in Latin America.

More info

“A woman with a voice is, by definition, a strong woman.” — Melinda French Gates