LatAm Tech Weekly

#190: SPECIAL EDITION - Trends - Artificial Intelligence by BOND

Weekly writing about what is happening in LatAm tech. By day, I work at Itau BBA advising mid-sized technology companies in their next strategic transaction. By night, I am reading and learning about technology in general (now, with a focus on AI). During the weekends, I’m writing the LatAm Tech Weekly.

If you have not subscribed yet, join the 12,500+ weekly readers by subscribing here!

Happy Sunday!

Let’s be honest — there was no escaping it. The must-read of the week was the new AI trends report from BOND Capital. Yes, that BOND Capital, the firm founded by none other than Mary Meeker — the original Queen of the Internet.

For those who need a refresher: Mary Meeker made her name as a top tech analyst at Morgan Stanley in the '90s, where she co-authored The Internet Report — basically the Bible of the dot-com era. She went on to release her iconic Internet Trends decks every year, packed with charts, stats, and insights that made even the most jaded execs sit up straight. Then, in 2018, she launched BOND Capital… and for the past six years? Radio silence.

Until now.

Last Sunday night, out of nowhere, the silence broke. I was lying in bed, battling my usual Sunday insomnia, when a message popped up in our group chat from the MD of Tech at Itaú BBA:

“This is a must-read.”

Curious, I clicked the link. Boom — 340 pages. My first thought? Too long. I’ll run it through ChatGPT.

Did that. Skimmed the summary. Meh.

Then I tried NotebookLM. Slightly better, but still missing the nuance.

So I sighed, gave in, and thought: Fine. I’ll read it myself.

I started. I fell asleep. In that sense, I guess it worked?

The next morning, I went for a run — and as part of my new routine, I tuned into the Daily Brief AI podcast. And what do you know? The episode was all about the BOND report. I was on the treadmill, and suddenly: BOOM. Graphs, insights, commentary — all the stuff I’d been hoping to extract from the bots. That’s when I decided:

I will read this thing. All of it. And I will summarize it. For you. In my own way.

So that’s what I did. I went through all 340 pages during this past week, highlighter in hand, old-school style. It took forever. But it was worth it. Because in a world where AI can summarize anything, sometimes what you really want is a human take — someone who’s read the thing, thought about it, and filtered it through a lens that actually makes sense for you…

So today, you’re getting Julia’s take on the BOND AI report.

Let’s dive in. And if you’re into this topic, I highly recommend doing the same. Yes, it’s long. But so is the future.

Let’s go.

“Knowledge is a process of piling up facts; wisdom lies in their simplification.” Martin H. Fischer

Imagine starting your week and discovering the internet no longer exists. Workflows, communication, governance — nearly every system we rely on would be disrupted. That’s how deeply the internet is embedded in modern life. Within the next decade, artificial intelligence may become just as foundational.

AI is no longer confined to research labs. It is rapidly becoming core infrastructure across industries — powering customer support, software development, scientific research, education, and manufacturing. Tools like ChatGPT have moved from experimental to essential, and the cost of deploying advanced models has dropped significantly. Both open-source and proprietary models are now widely accessible, enabling individuals, startups, and enterprises to build and deploy with minimal friction.

Technology leaders are integrating AI into every layer of their products. Copilots, assistants, and autonomous agents are reshaping how users interact with software. The interface itself is evolving — in real time.

Behind the scenes, infrastructure investment is scaling rapidly. Cloud providers, chipmakers, and hyperscalers are committing record capital to support real-time, high-volume inference. This includes not only chips, but also data centers, networking systems, and energy infrastructure. As AI moves closer to the edge — into vehicles, farms, labs, and homes — the boundary between digital and physical infrastructure is becoming increasingly blurred.

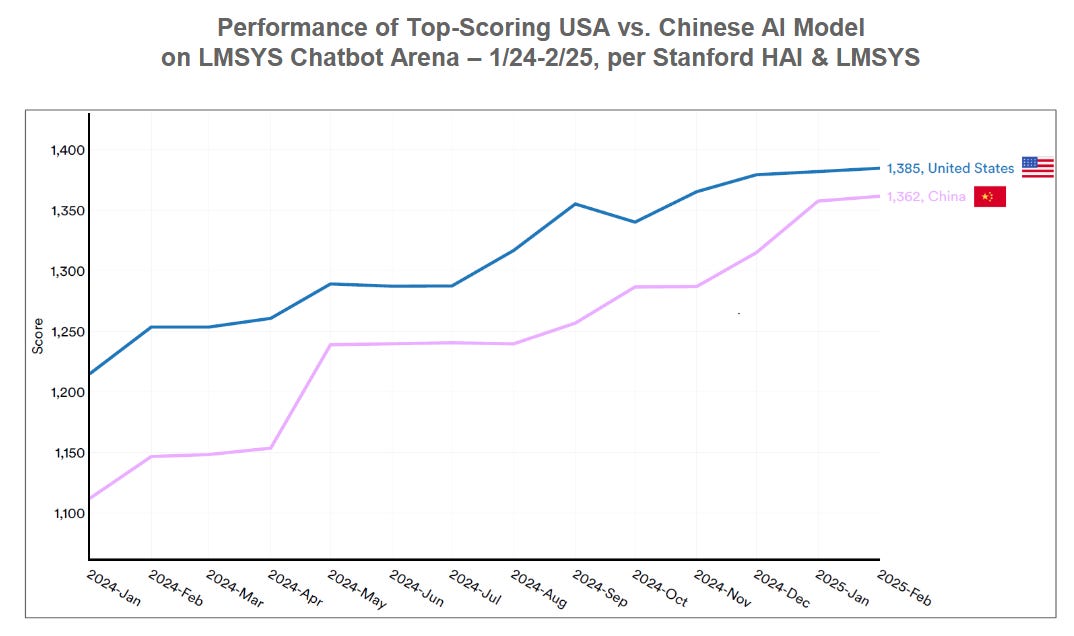

At a global level, the race to develop and deploy frontier AI systems is increasingly defined by strategic competition between the United States and China. U.S. companies currently lead in model innovation, custom hardware, and cloud-scale deployment. Meanwhile, China is advancing rapidly in open-source development, national infrastructure, and state-backed coordination. Both nations view AI not only as an economic driver but also as a lever of geopolitical influence.

These parallel AI ecosystems are accelerating the global push for technological sovereignty, security, and speed.

The systems being built today — and who controls them — will shape the future of work, innovation, and global power. AI is no longer just a tool. It is becoming the infrastructure of the future.

"Study the past, if you would divine the future."

— Confucius

Going Way Back: A Brief History of Knowledge Distribution (and Why It Matters for AI)

Before we dive into the future, let’s rewind a bit. Because to understand where we’re headed with AI, it helps to look at how we’ve shared and scaled knowledge over time:

1440 – The Printing Press: Gutenberg’s invention democratized access to information. Books went from rare artifacts to mass-produced tools of enlightenment.

1993 – The Public Internet: Suddenly, knowledge wasn’t just printed — it was searchable, clickable, and global.

2022 – Generative AI Goes Public: ChatGPT launches in November, and the way we interact with information changes again — this time, it talks back.

Each of these moments reshaped how humans learn, create, and make decisions. And AI? It’s the next chapter.

Let’s Get Our Terms Straight (if you are an expert, skip this section)

Before we go further, a quick glossary — because if we’re going to talk about AI, we should at least agree on what we mean:

🧠 Artificial Intelligence (AI)

The umbrella term. It refers to any technique that enables machines to mimic human intelligence — like recognizing speech, making decisions, or recommending your next binge-watch.

🤖 Machine Learning (ML)

A subset of AI. Instead of being explicitly programmed, machines learn from data. Think: showing a model thousands of cat and dog photos until it figures out the difference.

🧬 Deep Learning

A more advanced form of ML that uses deep neural networks — structures inspired by the human brain — to handle complex tasks like facial recognition, language translation, or autonomous driving.

🧠 Neural Networks

These are the “brains” behind deep learning. They process information in layers, refining their understanding at each step. The more layers, the “deeper” the learning.

🗣️ Natural Language Processing (NLP)

The branch of AI that helps machines understand and generate human language. It’s what powers chatbots, translation tools, and yes — ChatGPT.

✍️ Generative AI

This is where things get creative. Generative AI doesn’t just understand — it produces. Text, images, music, code… you name it. All from a simple prompt.

A Quick Timeline: From Theory to 800 Million Users

Let’s walk through the key moments that brought us here:

1950 – Alan Turing proposes the Turing Test to evaluate a machine’s ability to exhibit human-like intelligence. (Yes, the same Turing who helped crack the Nazi Enigma code.) We could say this was the start of AI.

1962 – An IBM developer creates a program that beats top U.S. checkers players.

1966 – Stanford researchers deploy the first robot capable of processing and reasoning about its own actions.

1967–1996 – AI Winter: Funding dries up, progress stalls, hype fades.

1997 – IBM’s Deep Blue defeats world chess champion Garry Kasparov.

2002 – The first robotic vacuum cleaner hits the market. (Shoutout to Roomba.)

2010 – Apple acquires Siri and integrates it into the iPhone 4S.

2014 – A chatbot named Eugene Goostman passes the Turing Test (sort of).

2020 – OpenAI releases GPT-3, but it’s only available via license.

2022 – ChatGPT launches publicly. The world takes notice.

And then… the floodgates open:

2023–2025 – A wave of innovation:

GPT-4 goes multimodal (text, image, code…)

Microsoft launches Copilot

Anthropic releases Claude

Apple introduces Apple Intelligence

Alibaba enters the race

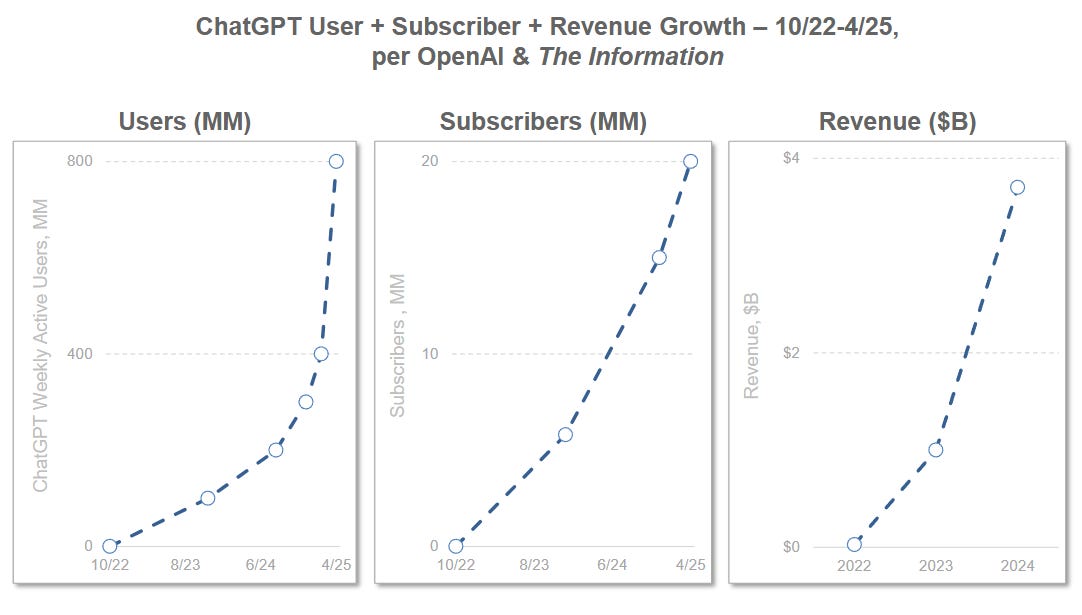

April 2025 – ChatGPT hits 800 million weekly users. Yes, weekly.

From printing presses to predictive text, we’ve always built tools to extend our thinking. But this time, the tools are starting to think back. And that changes everything…

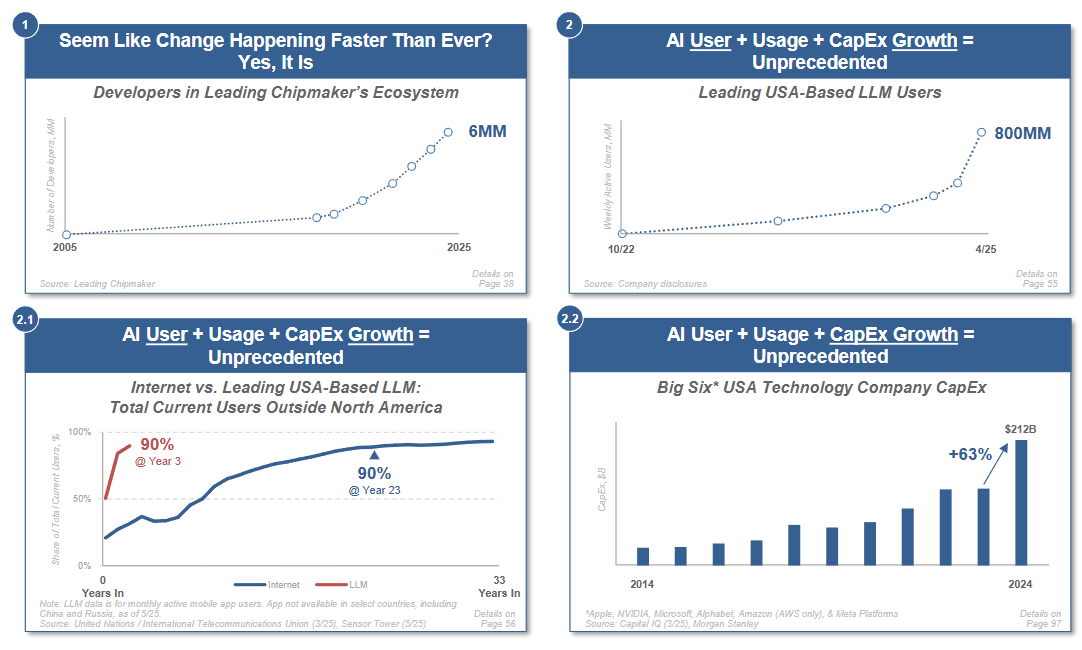

Change Is Happening Faster Than Ever — Literally

Let’s not sugarcoat it: saying the world is changing fast is an understatement. The pace of transformation — especially in AI — is unlike anything we’ve seen before.

Take this in:

There are now over 800 million weekly users of large language models (LLMs).

90% of ChatGPT users are outside the U.S. — a milestone the internet only reached in its 23rd year. ChatGPT did it in three.

Developer adoption is skyrocketing.

And capital expenditures? Projected to hit $212 billion in 2024.

Notice how the global curve for ChatGPT adoption is nearly vertical compared to the slow, steady climb of the early internet. This wasn’t a U.S.-first rollout — it was global from day one.

And here’s the kicker: even as infrastructure costs rise, inference costs per token are falling. That means performance is improving while access is getting cheaper — a rare combo in tech.

To borrow a sports analogy from the report:

Yes, athletes are still breaking records — but now they’re doing it with better data, better inputs, and better training. AI is no different. The tools are getting sharper, and the people using them are getting smarter.

The Time Is Now

Since 2010, the compute required to train AI models has grown by 360x. But it’s not just about brute force — algorithmic improvements alone have driven a 200% boost in model performance. This is what’s powering the breakthroughs behind models like GPT-4, Claude, and xAI.

And if you’re wondering how fast this is all moving:

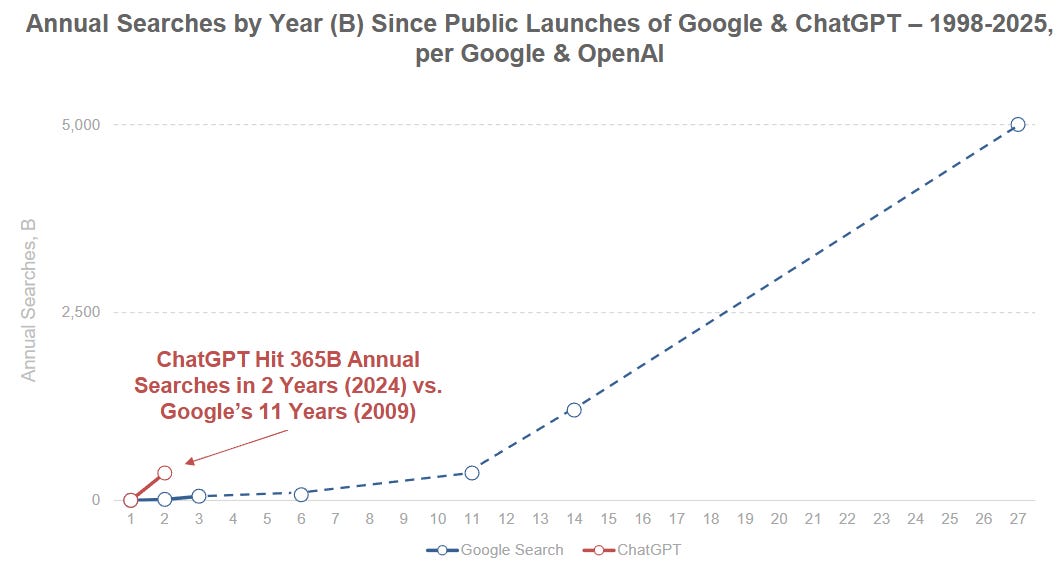

ChatGPT hit 365 billion annual searches in just two years.

For comparison, it took Google 11 years to reach that same milestone.

Emerging AI Applications

This isn’t just about chatbots and code completion anymore. AI is already being applied in ways that feel like science fiction:

🧬 Protein folding — we now know the structure of nearly every protein in the human body.

🧫 Cancer detection — AI is helping spot patterns invisible to the human eye.

🤖 Robotics — from warehouse automation to humanoid prototypes.

🌍 Universal translation — real-time, cross-language communication is here.

🎬 Digital video creation — AI is writing, directing, and producing content.

And that’s just the beginning.

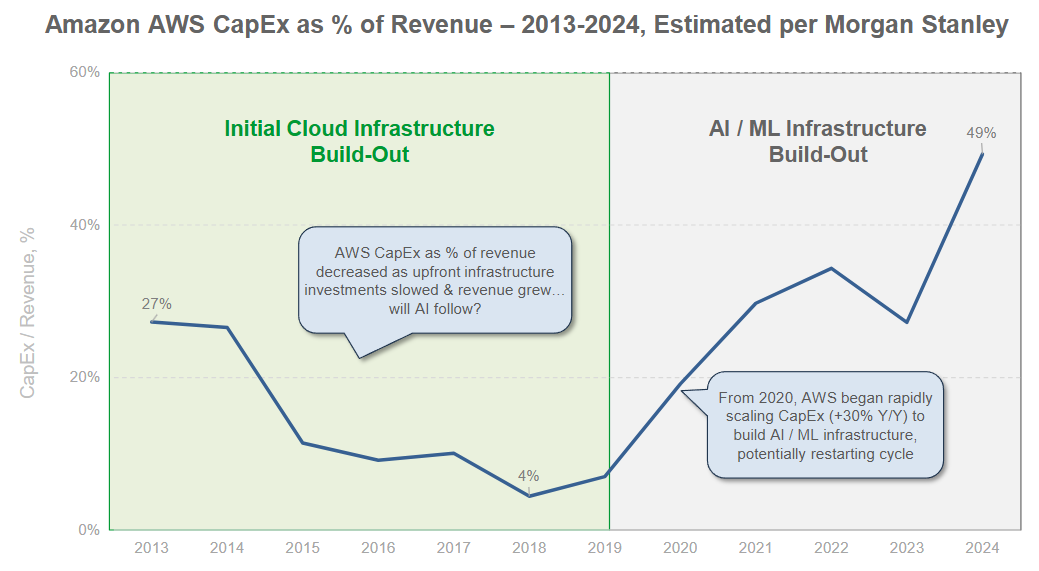

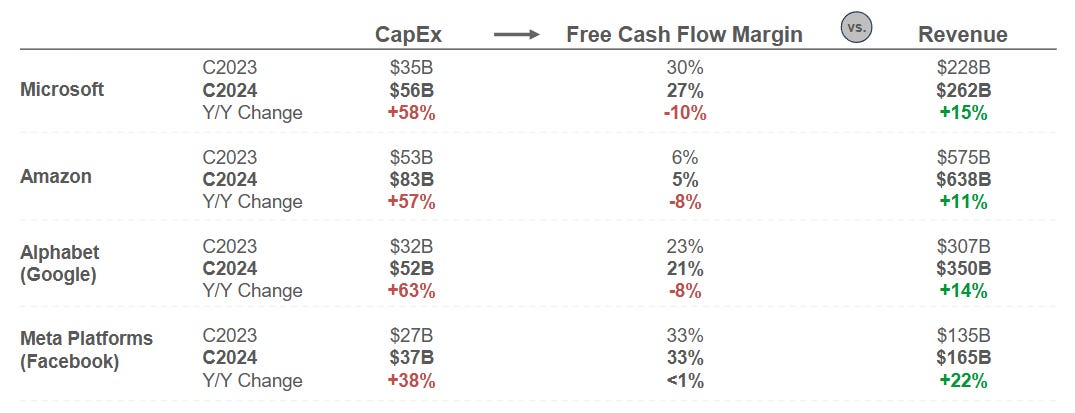

Capex expense by big tech on AI is MUCH higher than what was invested in CLOUD

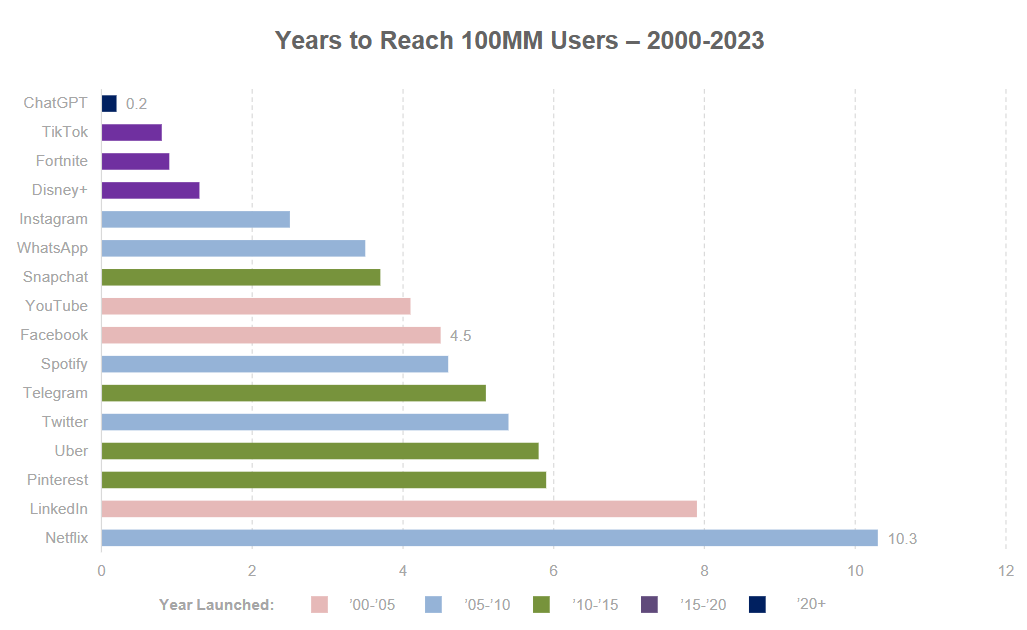

AI User Growth

8x to 800MM users in 17 months

Relative growth is amazing…

AI Computing Economics: Where the Money’s Going (and Why It Matters)

If you want to understand how AI is evolving, follow the money. And right now, most of that money is going into compute — the raw power needed to train and run large language models (LLMs). Training a frontier model today can easily cost over $100 million. And that’s just the beginning. Around that core are other high-cost layers: research, data acquisition, hosting, salaries, and go-to-market operations.

But here’s the shift: while training costs are still massive, a growing share of AI spend is moving toward inference — the cost of running models in real time, at scale.

What Is Inference?

Think of it as the deployment phase of AI.

· Training is when the model learns — like feeding it thousands of labeled images of cats and dogs.

· Inference is when it sees a new image and says, “That’s a cat.”

Inference happens constantly. Training happens occasionally. So over time, inference becomes the bigger cost driver — especially as usage explodes.

AI COST FLYWHEEL: The broader dynamic is clear: lower per-unit costs are fueling higher overall spend. As inference becomes cheaper, AI gets used more. And as AI gets used more, total infrastructure and compute demand rises – dragging costs up again. The result is a flywheel of growth that puts pressure on cloud providers, chipmakers, and enterprise IT budgets alike.

In the short term, it’s hard to ignore that the economics of general-purpose LLMs look like commodity businesses with venture-scale burn.

As models get better, usage increases – and as usage increases, so does demand for compute. We’re seeing it across every layer: more queries, more models, more tokens per task. The appetite for AI isn't slowing down. It’s growing into every available resource – just like software did in the age of desktop and cloud. Improvements in hardware efficiency are critical to offset the strain of increasing AI and internet usage on our grid. So far, though, they have not been enough.

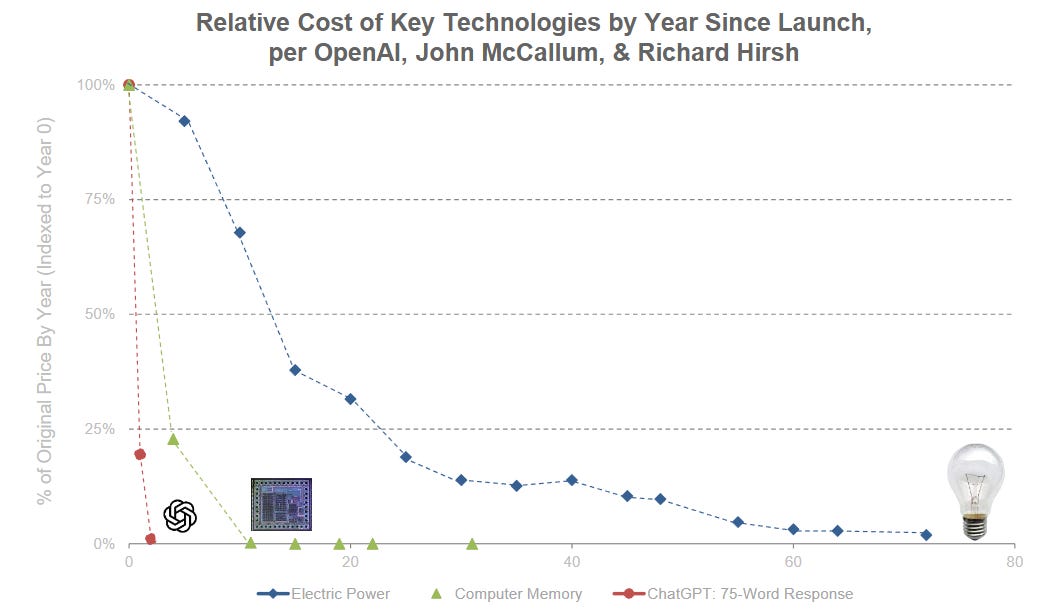

Energy required per LLM Token (Joules) decreased -105,000x over 10 years.

Efficiency gains are happening faster in AI vs. Prior technologies.

Where’s the Money Flowing?

AI monetization is already taking shape across three layers:

Chips: NVIDIA (still dominant), but competition is heating up —Google TPU (PUs are an application-specific integrated circuit (ASIC), a chip designed for a single, specific purpose: running the unique matrix and vector-based mathematics that’s needed for building and running AI models) // AWS Trainium chips are a family of AI chips purpose built by AWS for AI training and inference to deliver high performance while reducing costs.

Compute Services: CoreWeave, Oracle AI, and others are scaling infrastructure to meet demand.

Data Layer: Companies like Scale AI and VAST Data are building the pipelines and platforms to feed the models.

Where Is Enterprise AI Monetization Headed?

To understand where enterprise AI monetization is going, it helps to ask a broader question: where is software itself consolidating? (Again, understanding the past is the best way to predict the future).

For decades, enterprise software followed a familiar playbook:

Build a specialized tool

Sell it to a niche vertical

Scale within that vertical

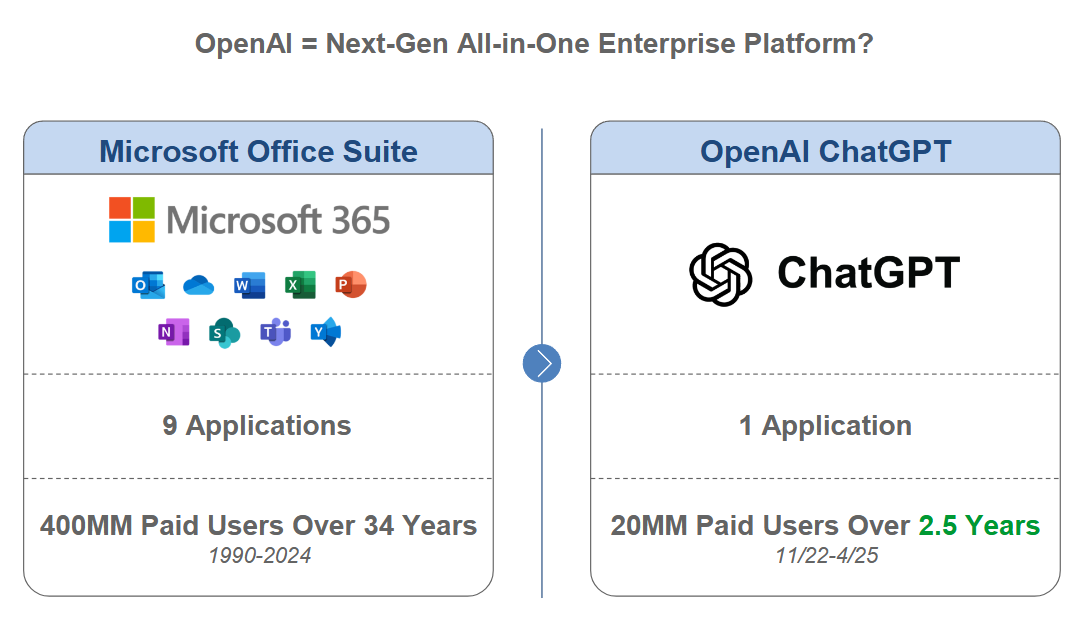

Then came the rise of horizontal platforms — systems that cut across industries and functions, combining productivity, search, communication, and knowledge management into a single interface. Think: Microsoft 365, Google Workspace, Salesforce.

Now, we’re seeing the same shift in AI.

Horizontal vs. Vertical: The New AI Stack

Horizontal platforms are embedding AI across the board:

Microsoft is rolling out Copilot across its entire suite — Word, Excel, Teams, Outlook.

Zoom and Canva are layering GenAI into user-facing workflows.

Databricks is infusing GenAI into its data and developer stack.

But here’s the twist: vertical players are moving faster than ever. They’re embedding AI directly into industry-specific workflows and fine-tuning models on proprietary data — giving them a sharp edge in relevance and performance.

So the question isn’t “platforms vs. specialists.” It’s:

Who can abstract the right layer, own the interface, and capture the logic of work itself?

The New Economics of Attention

In the AI era, monetization won’t just follow usage. It will follow attention, context, and control.

Who owns the interface where work happens?

Who controls the data layer that feeds the models?

Who captures the user’s intent at the moment of action?

These are the new battlegrounds. And the winners won’t just be the ones with the best models — they’ll be the ones who own the flow of work.

What is happening now?

The gap between the biggest, most powerful models and smaller, more efficient alternatives is narrowing. Developers are no longer locked into a single provider. Instead, they’re spreading their bets across ecosystems — choosing the best-fit model for their technical and financial needs.

This is creating a more pluralistic AI landscape, where flexibility and cost-efficiency are starting to matter as much as raw power.

We’ve never seen this many founder-led (or founder-assisted — looking at you, Apple) companies with $1 trillion+ market caps, 50%+ gross margins, and free cash flow — all going after the same opportunity at the same time. Add in the geopolitical tension between the U.S. and China, and you’ve got a high-stakes race playing out in real time.

Technology disruption has a long-repeating rhythm: early euphoria, break-neck capital formation, bruising competition, and – eventually – clear-cut winners and losers.

Is AI a Bubble?

Let’s address the trillion-dollar question: is AI a bubble?

History (again) reminds us that some of today’s most iconic tech giants were once on the brink — and looked, frankly, like terrible bets. But long-term value often emerges from short-term chaos. A few examples worth remembering:

Apple was nearly bankrupt in 1997, with a market cap of just $1.7B. Today? $3.2T.

Amazon lost $545M in Q4 2000. Its stock dropped over 80% that year. At its lowest in 2001, it was worth $2.2B — while serving 23 million customers. It burned $3B in its first 27 quarters. In its most recent 27? $176B in net income. Current market cap: $2.2T.

Google, pre-IPO in 2004, was spending 22% of its revenue on capex — a shocking figure at the time. It went public at $23B. Now? $2.0T.

Uber burned $17B between 2016–2022 before finally turning free cash flow positive in 2023. IPO valuation: $82B. Today: $189B.

Each of these companies tested the limits of investor patience — burning cash aggressively, building data-driven network effects, and doubling down on product and tech. In the end, they proved that valuation is (still) the present value of future free cash flows.

The open question: which side of that equation will today’s AI hopefuls land on?

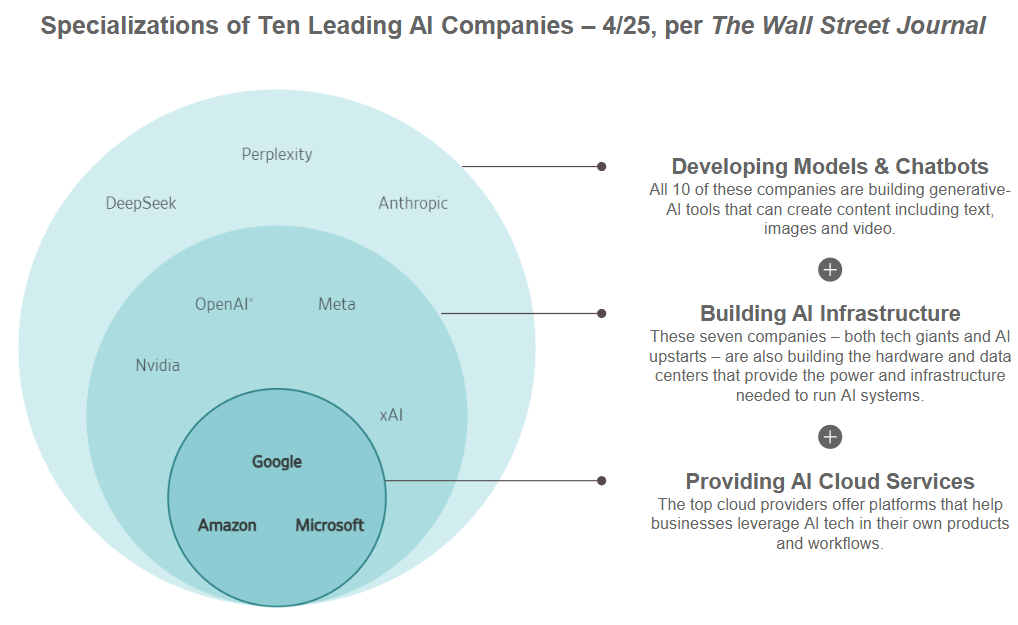

The AI Landscape

How are the players reacting?

Tech Incumbents:

The incumbents aren’t sitting still. They’re optimizing distribution, embedding AI into their existing platforms, and leveraging scale like only trillion-dollar companies can.

Let’s talk reach:

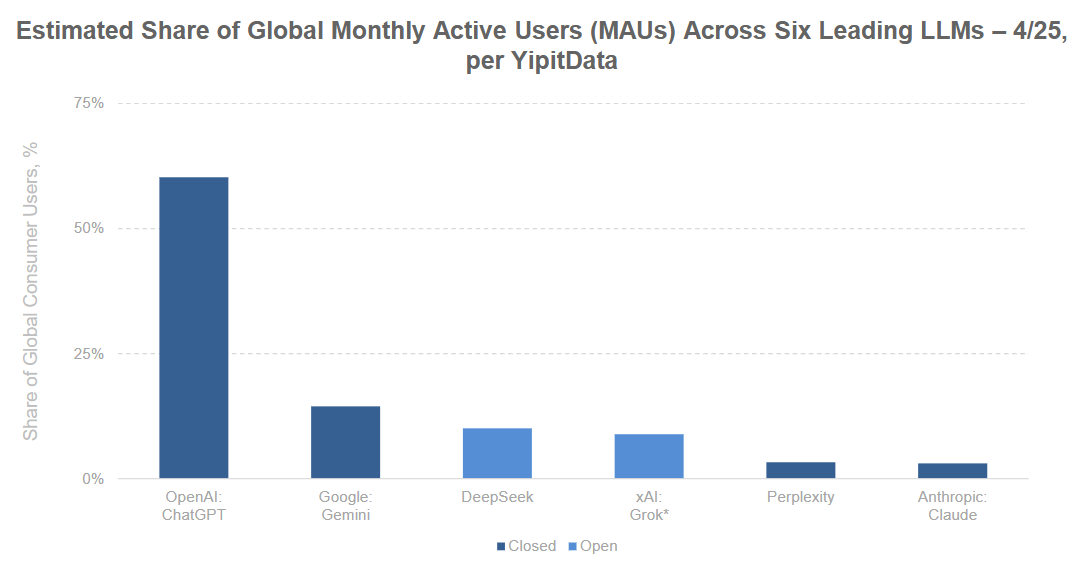

ChatGPT has 800 million users.

Google Search 4.9 billion users.

Meta 3.5 billion users.

Apple 2.35 billion active devices.

And they’re moving fast:

Microsoft launched Copilot across its suite.

Alphabet rolled out Gemini.

Apple is (quietly) integrating AI across its ecosystem.

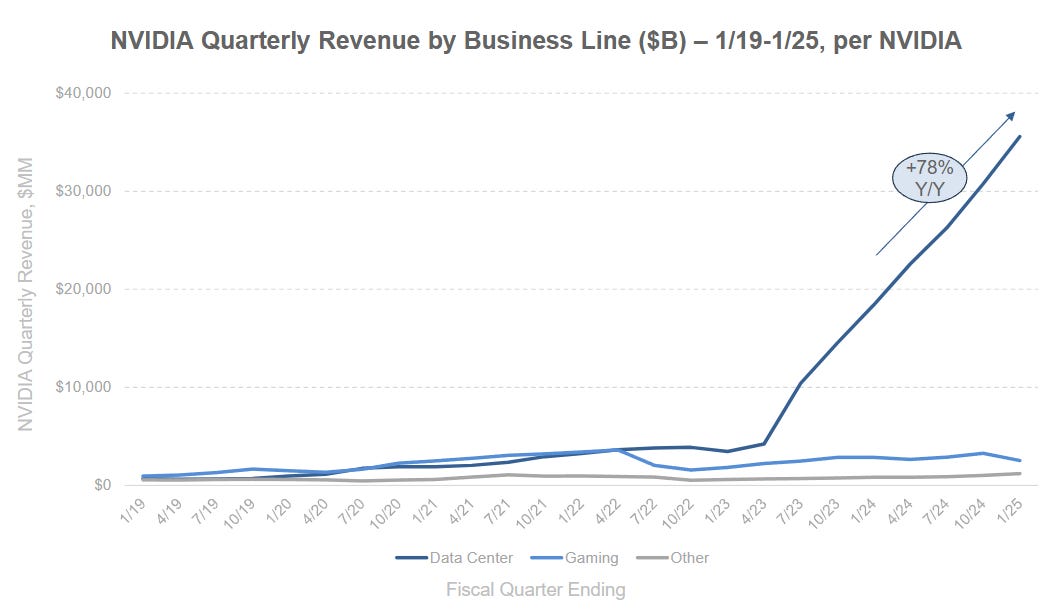

“AI Revenue” by big tech companies is starting to show up…

Microsoft reported AI revenue up +175% YoY, hitting $13B.

xAI (Elon’s venture) saw material revenue growth in 2025.

Palantir’s U.S. commercial business — driven by its AIP platform — grew 65% YoY.

So, is AI a bubble? Maybe. But if history is any guide, bubbles aren’t always bad. They’re often the messy, volatile prelude to something enduring. The trick is knowing which players are building for the long term — and which are just riding the wave.

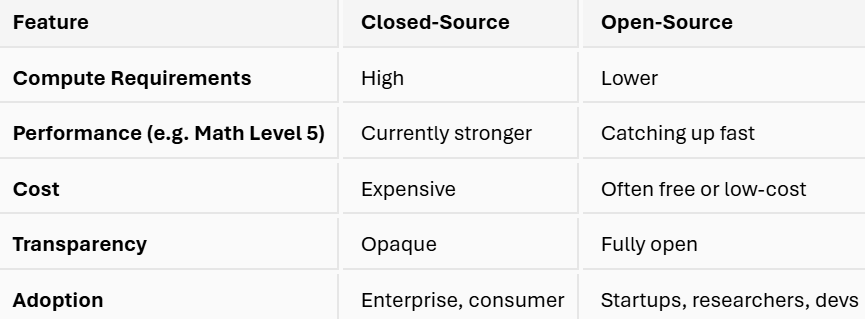

Closed-Source vs. Open-Source: Two Roads, One Race

From 2012 to 2018, modern machine learning was largely open-source — a product of academic collaboration and shared curiosity. But in 2019, something shifted. When OpenAI released GPT-2 with restricted access to its weights, it marked the beginning of a new era: the rise of closed-source AI.

Since then, powerful models like GPT-4 and Claude have been developed behind closed doors. These models require massive compute, proprietary datasets, and deep pockets — but they deliver high performance, seamless UX, and enterprise-grade reliability. Unsurprisingly, they’ve become the go-to for businesses, consumers, and governments alike.

The tradeoff? Opacity.

No access to weights. No visibility into training data. No insight into fine-tuning methods. What started as open research has become a gated product experience — delivered via APIs, protected by legal firewalls, and monetized at scale.

The Open-Source Resurgence

But the story doesn’t end there. As LLMs mature and competition heats up, open-source AI is making a comeback.

Models like Meta’s Llama and Mistral’s Mixtral are:

Freely available

Cost-effective

Surprisingly capable

They’re being used by startups, researchers, and developers to build apps, agents, and pipelines that once required closed APIs. Platforms like Hugging Face have made it frictionless to access and deploy these models — turning open-source AI into the garage lab of the modern tech era.

And globally? China is leading the open-source race.

As of Q2 2025, it has released three major open models:

DeepSeek-R1

Alibaba Qwen-32B

Baidu Ernie 4.5 (to be open-sourced by June 30)

So… Which Is Better?

Well, it depends.

The real question isn’t which one wins — it’s who gets to shape the future of AI.

Closed models are dominating the market.

Open models are fueling innovation and sovereignty.

Two philosophies.

Openness vs. control.

Speed vs. safety.

Access vs. optimization.

And both are rewriting the rules of what’s possible.

Will All of Us Lose Our Jobs?

No — not quite yet.

Technology has always reshaped the nature of work. From steam engines to spreadsheets, every wave of innovation has forced us to adapt. AI is no different — just faster.

You’ve probably heard the line:

“You won’t lose your job to AI. You’ll lose it to someone using AI.”

And honestly? That’s not far off.

Yes, every job will be affected. Some will disappear. Others will be created. But all of them — from finance to design to logistics — will be transformed. Especially roles that rely on processing structured data and making rule-based decisions. That’s generative AI’s sweet spot.

Since ChatGPT’s public debut in November 2022, we’ve gone from high school-level reasoning to near PhD-level capabilities. That’s in just three years. The pace is staggering — and the implications are real.

From Labor to Compute

In this new landscape, the unit of labor may shift from human hours to computational power. The availability and quality of certain types of work could increasingly depend on data centers and foundation models. That’s led to visions of an “agentic future,” where AI agents take over many white-collar roles.

But let’s not jump to dystopia just yet.

History shows that humans adapt. Every major technological leap — from the assembly line to the cloud — has created new jobs, even as it made others obsolete. The difference now is speed.

Humans Still in the Loop

Even in a future where AI agents handle much of the execution, humans will still play a critical role — not as doers, but as overseers, trainers, and guides.

Picture this:

Factories where people teach robots fine motor skills.

Offices where workers provide reinforcement learning feedback to improve AI behavior.

This isn’t sci-fi. Companies like Physical Intelligence and Scale AI are already building businesses around this exact model.

Yes, the idea of humans reconfigured to train machines might sound dystopian. But so did the image of rows of office workers staring at LED screens all day — until it became normal.

So no, we’re not all losing our jobs.

But we are all getting new ones — whether we’re ready or not.

General news:

PayPal has entered Brazil’s acquiring market. Announced at VTEX Day 2025, PayPal now processes payments end-to-end in the country, opening new opportunities for BNPL and AI-powered tools. 🇧🇷

Ualá integrated its prepaid cards with Google Wallet, enabling secure contactless payments via Android devices. Ualá plans to add credit card support soon to expand its digital payment ecosystem. 🇦🇷

Brazil’s Central Bank proposal to cap credit card interchange fees could lift profits for acquirers like Stone, PagSeguro, and Mercado Pago by up to 8%, per Itaú BBA. Banks with dual roles would see smaller impacts. Gains are expected to be temporary as competition intensifies. 🇧🇷

Builder.ai collapsed after raising $450M by falsely claiming to automate app development with AI. Bloomberg revealed the British startup was using 700 Indian engineers to do manual coding. Backers included Microsoft and Qatar’s sovereign fund. It has since filed for insolvency. 🇬🇧

Solo Network posted R$700M in 2024 revenue, driven by cloud and cybersecurity services. Ranked on the FT Americas Fastest-Growing list, Solo aims for 30% growth in 2025 and continues investing in innovation and talent. 🇧🇷

Deals:

FCamara acquired 60% of e-commerce specialist Avanti for R$20M. The move is set to boost FCamara’s digital retail operations by adding R$40M in revenue by 2025. Avanti, a top VTEX partner, will maintain its independent structure while gaining access to FCamara’s cloud and AI capabilities. 🇧🇷

Finnecto raised $1.7M in pre-seed funding to scale its AI-powered SaaS platform for automating spend and vendor payments across Latin America. The platform cuts operating expenses by up to 80%. 🇨🇱

OmniChat raised R$50M to launch Whizz, a no-code AI agent platform for automating sales across WhatsApp, Instagram, and more. OmniChat serves over 500 brands with integrations to major e-commerce platforms. 🇧🇷

General news:

inDrive is expanding aggressively in Brazil, targeting 100 new small and mid-sized cities. Already serving 17M users across 200 cities, it plans to grow into logistics, small business delivery, and fintech for drivers. 🇧🇷

Deals:

Speedata raised a $44M Series B to bring its custom APU chips to market, targeting big data and AI workloads. The Israeli startup claims its chips outperform GPUs for data analytics and plans to debut them at Databricks' Data & AI Summit this month. 🇮🇱

UAUBox acquired beauty subscription startup Experimentaí, expanding its wellness ecosystem. UAUBox plans to relaunch the brand with improved logistics and marketing, targeting Gen Z consumers. 🇧🇷

Principia raised R$190M to scale its edtech platform in Brazil. The platform combines academic management and a “zero delinquency” solution already used by 600+ institutions and 500K+ students. 🇧🇷

DLocal is acquiring AZA Finance for $150M to expand into Africa. The move will broaden DLocal’s FX and cross-border payment solutions beyond Latin America. 🇺🇾

General News:

Itaú partnered with Chilean fintech Khipu to launch a joint payment reconciliation service — the first such co-marketed product between a major bank and fintech in Latin America. 🇧🇷🇨🇱

QuintoAndar will shut down its tenant guarantee service, QuintoCred Garantia, by October 2025.

Klap launched Checkout Flex, Chile’s first gateway supporting Apple Pay and Google Pay. The tool integrates directly with ecommerce platforms to boost conversion rates and improve user experience. 🇨🇱

Brazil faced 356 billion cyberattack attempts in 2024 — nearly 40% of LatAm’s total. In response, the government launched a National Cybersecurity Plan with public-private collaboration through 2031. 🇧🇷

Pix Automático launches June 16 in Brazil with pioneers like Amazon, Netflix, Spotify, and Disney+. The feature will enable secure recurring payments via Pix, aiming to replace cards and boletos. 🇧🇷

Deals:

BS2 acquired VoucherPay to expand its cross-border Pix payment services. The move supports BS2’s goal to process R$100M via VoucherPay by year-end and scale internationally. 🇧🇷

Simetrik raised $30M in a round led by Goldman Sachs Alternatives to fuel global growth, with 25% of the funds allocated to Brazil. 🇨🇴🇧🇷

CloudWalk acquired control of SF3 and renamed it CloudWalk Financeira after securing Central Bank approval — strengthening its financial services capabilities in Brazil. 🇧🇷

General news:

Pix Parcelado will launch in September 2025, letting Brazilians split payments via Pix — “credit without cards.” 72% of consumers are interested, but only 1/3 of retailers are aware of it. 🇧🇷

Omie launched an integration that lets Brazilian entrepreneurs run their ERP entirely through WhatsApp — managing balances, inventory, and orders via simple chat commands. 🇧🇷

Brazil’s government will soon launch "Redata," a national policy to attract AI and data center investments — leveraging Brazil’s renewable energy advantage. 🇧🇷

OpenAI is rolling out new ChatGPT business features — including document querying and meeting transcription — adding Google Drive and Dropbox integrations. 🇺🇸

Nuvemshop integrated Loggi into its Nuvem Envio platform, giving merchants easy access to LoggiPonto drop-off points nationwide. 🇧🇷

Deals:

Crabi raised $13.6M led by Kaszek and Ignia — expanding its AI-driven digital auto insurance across Mexico. 🇲🇽

SRM Asset launched SRM Venture Studio, targeting three new fintechs in 2025 — supported by a R$500M fund. 🇧🇷

General news:

Mercado Livre slashed its free shipping threshold in Brazil from R$79 to R$19 and cut logistics costs for sellers — countering Shopee and TikTok Shop. 🇧🇷

Zig launched Zig Mesas, an AI-driven restaurant management platform — already live in 100+ venues and aiming for R$240M in transactions this year. 🇧🇷

Deals:

Circle debuted on the NYSE — stock soared over 170%, raising $1.1B and valuing the USDC issuer at $18.8B. 🇺🇸

Visa Conecta launched in Brazil to tap into the Open Finance and Pix ecosystem — with Payment Initiation Provider approval pending. 🇧🇷

You will see below an updated list of events, including for the second half of the year. If I forgot your event, and you want to include it - please sure to send those my way asap!

ABVCAP Experience 2025

Location: São Paulo, SP

Date: June 9–12, 2025

Description: Brazil’s premier private capital event, ABVCAP Experience brings together over a thousand delegates, including national and international LPs, for networking and discussions on the latest trends in private equity and venture capital. The event features LP Day, investment rounds, and panels on industry developments.

More infoChile Digital 2025

Location: Santiago, Chile

Date: June 10

Description: The third edition of the “Digital Hub of the Americas” summit takes over the CEPAL headquarters with discussions on connectivity, data centers, private 5G networks, and public policies aiming to establish Chile as the digital backbone of Latin America.

More InfoFEBRABAN Tech

Date: June 10-12

Location: São Paulo

Description: FEBRABAN Tech is a fundamental event for the financial sector, bringing together banks, fintechs, financial institutions and experts to debate the innovations that are shaping the future of the market. Held annually by the Brazilian Federation of Banks (FEBRABAN), the event reached a record of 55 thousand visitors in 2024.

Cubo Conecta 2025

Date: September 2025 (exact dates to be announced)

Location: São Paulo, SP

Description: Celebrating its 10th anniversary, Cubo Conecta is the flagship event of Cubo Itaú, bringing together thousands of entrepreneurs, investors, and innovation leaders from across Latin America. The event offers over 90 hours of content and facilitates more than 5,000 digital connections, highlighting the potential of the technology and innovation ecosystem in the region.

Brazil Climate Summit 2025

Date: September 13–14, 2025

Location: New York, NY, USA

Description: The Brazil Climate Summit focuses on Brazil's role in the global green transition, emphasizing the importance of private sector involvement and international capital to accelerate low-carbon businesses. The event gathers leaders from various sectors to discuss sustainable development strategies.

More infoGartner CIO & IT Executive Conference 2025

Date: September 22–24, 2025

Location: São Paulo, SP

Description: A gathering of CIOs and IT leaders to discuss digital transformation, organizational leadership, and innovation strategies across industries.

More infoWeb Summit Lisbon 2025

Date: November 10–13, 2025

Location: Lisbon, Portugal

Description: One of the world’s most influential tech conferences, Web Summit Lisbon connects 70,000+ attendees from startups, enterprises, and media to discuss trends shaping the tech industry.

More infoBrazil Tech Summit 2025

Date: December 9, 2025

Location: São Paulo, SP

Description: Part of the Global Startup Ecosystem Series, Brazil Tech Summit brings together entrepreneurs, government leaders, and investors to foster tech-driven innovation across Latin America.

More info

"Study the past, if you would divine the future."

— Confucius