LatAm Tech Weekly

228: VC Fund Performance Q4 2025, Mega IPOs, NVIDIA GTC, deals of the week... and much more!

Weekly writing about what is happening in LatAm tech. By day, I am part of the corporate development team at Itau Unibanco. By night, I am reading and learning about technology in general (now, with a focus on AI). During the weekends, I’m writing the LatAm Tech Weekly. And obviously, always running!

If you have not subscribed yet, join the 14,700+ weekly readers by subscribing here!

Happy Sunday!

This week was — as always — a busy one on the AI front. That said, I’ve leaned quite heavily on AI in the intro section over the past few weeks, so I’m switching things up and returning to the newsletter’s core focus: VC, startup fundraising, and IPOs.

With that in mind, you’ll find all the key AI updates in the dedicated AI section, as well as across the news coverage throughout the week.

If you’ve been following along regularly, you may have noticed that — due to time constraints — it’s been a while since I last published the Wednesday edition of Startups to Watch & Tech Talents with Pedro Mesquita. To make up for that, I’m including the latest highlights from this section at the end of today’s intro.

So, without further ado — let’s dive in.

Venture returns are getting even more unequal — and timing still matters

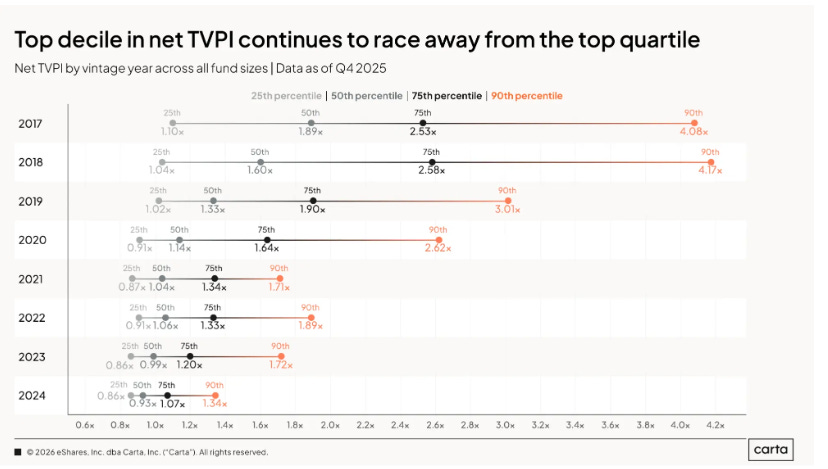

A very good read this week was Carta’s new report - VC Fund Performance for Q4 2025. One thing the data makes very clear: venture capital is becoming even more of a winner‑takes‑most game.

Across every vintage from 2017 to 2024, the majority of returns have been driven by a small number of outlier funds. The gap between good and great funds is far wider than the gap between average and below average. Take the 2019 vintage: funds at the 90th percentile show a 3.0x TVPI, versus 1.9x at the 75th percentile and 1.33x at the median. The jump from “top quartile” to “top decile” is larger than everything below it combined. The pattern repeats across vintages — and in some years it’s even more extreme (in 2017, top‑decile TVPI reached 4.1x, versus 2.5x at the top quartile).

That’s the structural reality of VC: a tiny number of companies — and funds — generate outsized outcomes, while most capital produces modest returns or none at all. Funds that catch one or two true outliers can comfortably offset the rest of the portfolio. Funds that don’t, can’t.

Recent vintages: still early, but momentum is shifting

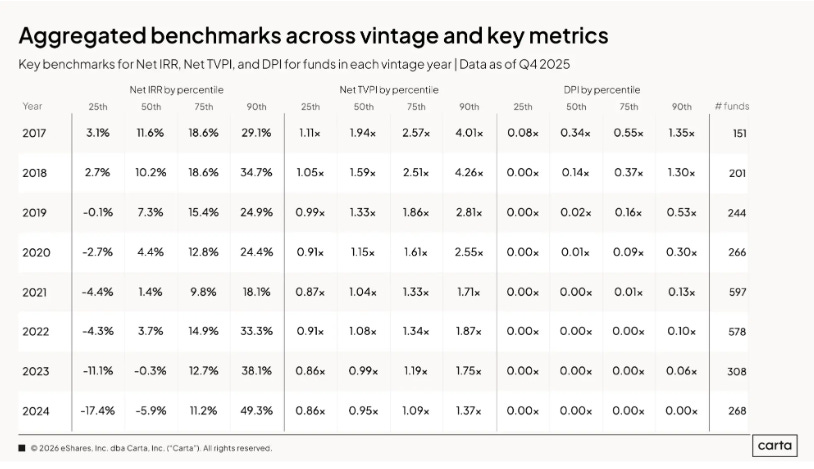

Despite the tough exit environment of the past few years, recent vintages are starting to show signs of life.

Median net IRRs for the 2021 and 2022 vintages have finally turned positive, now at 1.4% and 0.7%, respectively — a textbook J‑curve dynamic after several years underwater. Older vintages (2017–2020) all sit above 4.2% median IRR, though those numbers have been drifting down as funds mature.

Interestingly, 2022 and later vintages are outperforming 2021 at the top end. At both the 75th and 90th percentiles, 2022, 2023 and even 2024 funds are now ahead of 2021. That reflects the post‑2021 valuation reset: funds deploying capital after the bubble burst are benefiting from more disciplined entry prices.

At the very top, 2024 funds stand out. The 90th percentile IRR reached 35.7%, the highest of any vintage tracked — and strong early IRRs are visible across fund sizes. Large funds (> $100M) in the 2024 vintage show a striking 77.8% top‑decile IRR, bucking the usual pattern where smaller funds dominate on returns.

Dry powder is still massive

Capital deployment is far from done. Recent vintages are sitting on a lot of unspent cash:

2025 funds still hold 72% of committed capital as dry powder

2024: 53% unspent

2023: 35% unspent

Together, these three vintages account for more than $19B in dry powder. That suggests two things: competition for quality assets will remain intense, and ultimate fund outcomes are still very much undecided.

Distributions remain slow — exits are the bottleneck

Returns on paper are improving, but cash back to LPs is still lagging. More than half of 2020 funds have started generating DPI, but for 2021–2023 vintages, fewer than one‑third have returned any capital at all. After 16 quarters, only 33% of 2021 funds had begun distributions — compared to 50% for 2019 and 60% for 2017 at the same point.

The reason is simple: exits have been scarce. IPO windows remain narrow, M&A has been selective, and liquidity timelines are stretching. LPs will likely need more patience with recent vintages, even as underlying portfolio values improve.

Market backdrop: healing, not booming

The broader venture market is slowly normalizing:

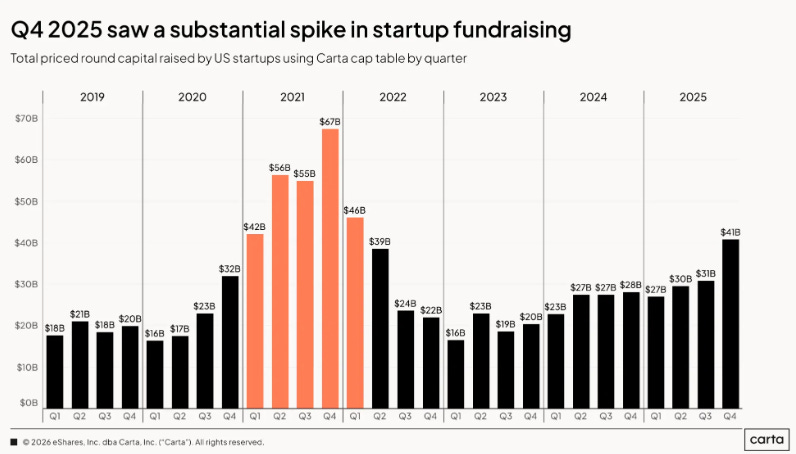

Q4 2025 fundraising hit $41B, the strongest quarter since early 2022

Down rounds fell to 14.5% of deals, the lowest in three years (though still elevated versus pre‑2021 levels)

Time between rounds is shortening again, especially from Seed to Series A

Graduation rates from Seed → A and A → B are rebounding

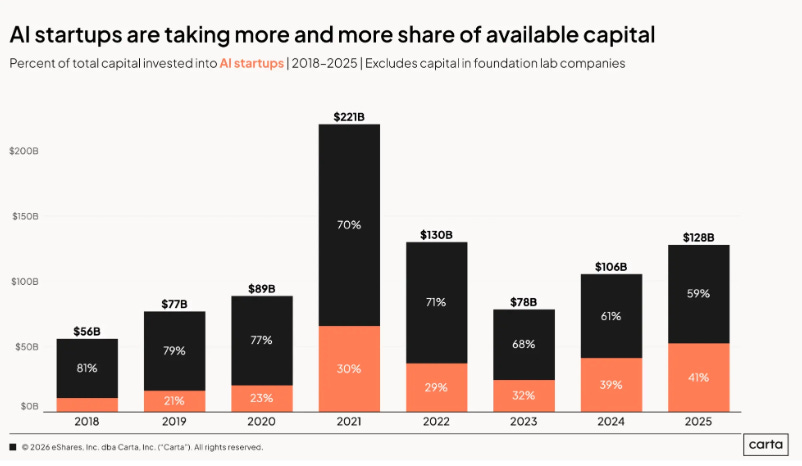

One number stands out above all: AI startups captured 41% of all capital raised in 2025, the highest share on record. That concentration is already showing up in fund‑level performance — particularly among top‑decile funds in the 2023 and 2024 vintages.

Bottom line: VC has always been unequal, but the data shows the gap widening. The best funds are pulling further ahead, post‑2021 vintages are quietly improving, and the next few years will be decisive as massive dry powder meets a slowly reopening exit market. In venture, as ever, the winners don’t just win — they win big.

For LatAm, this data reinforces a familiar but increasingly important reality: regional outcomes will be driven by a very small number of funds and companies that truly break out at global scale. As global VC becomes more top‑heavy, the bar for standout performance rises — and that matters in an ecosystem where exits are scarcer, fund sizes are often smaller, and access to late‑stage capital is uneven. The vintages deploying after the 2021 reset are structurally better positioned, but only managers who combine disciplined entry prices with exposure to global themes (notably AI, fintech infrastructure, and cross‑border platforms) are likely to reach the top decile where returns really concentrate. For LPs backing LatAm funds, the implication is sharper selection: being “above average” isn’t enough anymore — almost all the value sits with the true outliers.

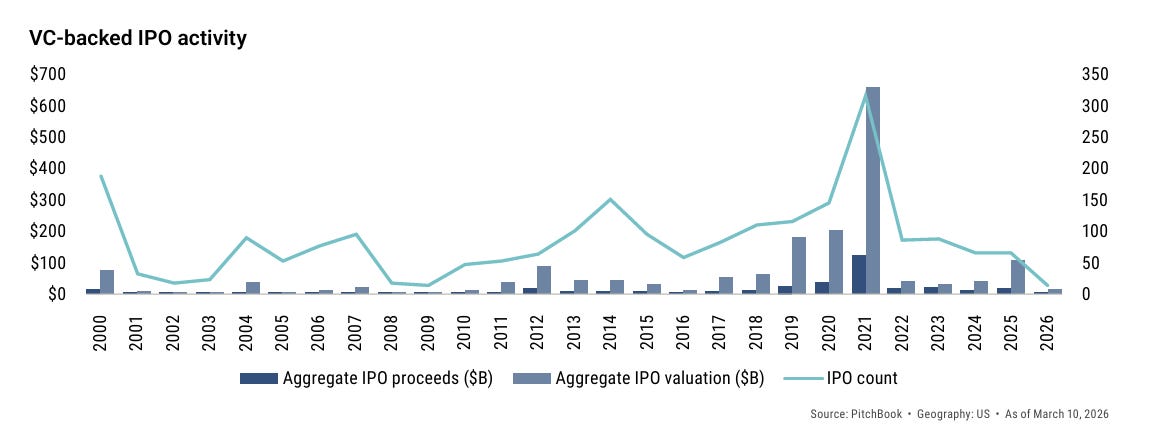

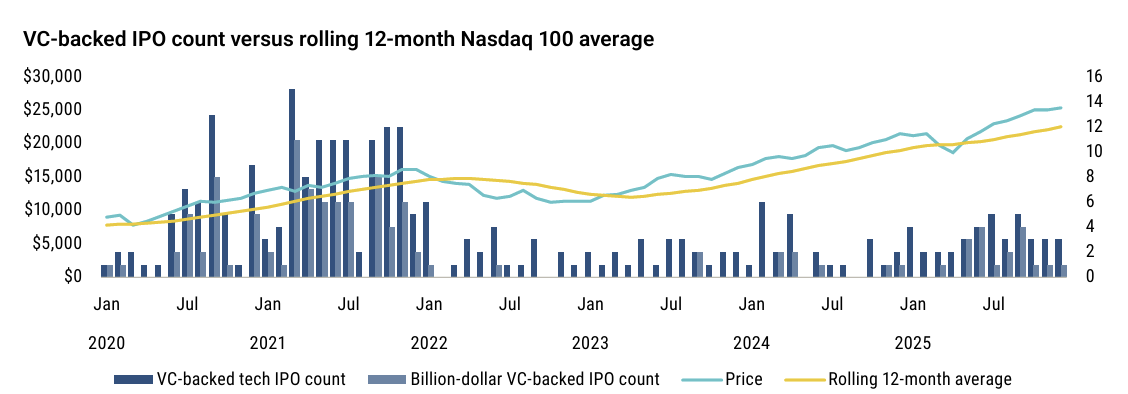

Moving on to Pitchbook, their recent analyst note on how mega IPOs could threaten the 2026 IPO Class was also relevant. PitchBook argues that the 2026 IPO market could be disproportionately shaped by a small number of potential mega listings, particularly from large, high-profile technology companies — including AI leaders such as OpenAI and Anthropic, as well as companies like SpaceX. These businesses could reach valuations in the hundreds of billions, and in some cases approach the trillion-dollar mark, making them significantly larger than the typical IPO cohort.

The central concern is a potential “crowding out” effect. Given the finite pool of public market capital, these mega IPOs could absorb a substantial share of investor demand, leaving less capital available for smaller or less differentiated companies. This dynamic could make it more difficult for mid-sized issuers to successfully price their offerings or sustain post-IPO performance, particularly in a market where investor selectivity remains high.

PitchBook also emphasizes that the broader IPO recovery is still fragile following the slowdown of the past few years. While activity has started to pick up, it remains uneven, with investors continuing to favor companies that demonstrate clear market leadership, strong fundamentals, and a credible path to profitability. In that context, the success of large, well-positioned issuers could reinforce this selectivity, further raising the bar for companies looking to go public.

As a result, the 2026 IPO class may become increasingly polarized, with capital and attention concentrated in a handful of standout companies, while the rest of the market faces a more challenging environment. The performance of these mega IPOs will likely play a critical role in shaping overall sentiment and determining whether the IPO window broadens or remains narrow.

STARTUPS TO WATCH & TECH TALENTS - Pedro Mesquita (click here to see full newsletter)

Overview

Startup Description: Insurance brokerage specializing in surety bond (Seguro Garantia), delivering clear, low‑friction policies that meet specific contractual, bidding, operational, and legal requirements.

Industry: InsurTech

Team Size: 1

Time in Stealth: 3 months

Founder Profile

Alfredo Cavalcante Neto - Founder at Garantis

Featured as a Stealth Founder in Tech Talents #36.

Founder Highlights: Serial Founder, Technical Founder, Top University, Ex-Corporate, Ex-Consultant, Unicorn Experience

Previous Experience: ex-Partner & Director of Finance and Operations at Latú Seguros, ex-Strategy and M&A Consultant at Porto Seguro, ex-Associate at BCG, Bachelor’s in Mechatronics Engineering from UNICAMP.

Headquarters: São Paulo, Brazil

Ask for an Intro: Click here

Overview

Startup Description: Atthena provides AI-optimized data infrastructure for Brazil’s capital markets, transforming CVM regulatory filings into a structured, relational, fully traceable database.

Industry: SaaS, AI

Team Size: 3

Time in Stealth: N/A

Founder Profile

Tiago Quadros - Co-Founder at Atthena

Founder Highlights: Top University, Ex-Corporate

Previous Experience: ex-Associate at Seneca Evercore, ex-M&A Analyst at Singular Partners, Bachelor’s in Economics from Insper.

Headquarters: São Paulo, Brazil

Co-Founder: João Terra

Ask for an Intro: Click here

General news:

• Nebius Group signed a deal with Meta to provide up to $12B in AI compute capacity by 2027, with potential expansion to $27B over five years as demand for GPU infrastructure accelerates. The agreement follows a $2B investment from Nvidia for an 8.3% stake and builds on contracts with Microsoft, reinforcing Nebius’ position as a key neocloud provider focused on AI workloads amid rising competition for data center capacity and energy. 🇺🇸

• Elon Musk is rebuilding xAI after most of its founding team exited, leaving only 3 of 12 co-founders as the company resets its structure and talent base to improve product execution. xAI has resumed aggressive hiring, including senior recruits from Cursor to strengthen its coding tools and close gaps with competitors in the developer ecosystem. 🇺🇸

Deals:

• Apple acquired video editing software firm MotionVFX, integrating its plugins, templates and visual effects into Final Cut Pro to strengthen Apple’s creative ecosystem. The deal, with undisclosed terms, aims to improve workflow efficiency and expand features for content creators while reducing reliance on third-party tools, reinforcing Apple’s push into subscription-based creative services and competition with Adobe. 🇺🇸

General news:

• QuintoAndar launched an official app within ChatGPT, enabling users to search for properties through natural language and expanding its distribution strategy toward conversational interfaces. The feature allows users to describe preferences via text or voice and receive personalized listings directly in chat, driving engagement with users performing 174% more property visits compared to traditional search flows. 🇧🇷

• Brazil’s INSS suspended new payroll-deductible loans from C6 Bank after an audit identified irregularities in at least 320,000 contracts involving additional charges such as insurance and service packages deducted from retirees’ benefits. The agency ordered the bank to reimburse approximately R$300M to affected beneficiaries and halt disputed charges, with lending remaining blocked until compliance is verified. 🇧🇷

• Andes Levers is expanding deployment of industrial exoskeletons at the El Pachón copper project, a $9.5B initiative with projected output of 400,000 tons annually. The technology reduces physical strain and cuts muscle fatigue by up to 44.5%, while complementary solutions such as smart bracelets improve workplace safety across mining, construction and energy sectors. 🇨🇱

• Ualá launched an investment advisory service in Mexico, allowing users to buy and sell US stocks with fractional ownership starting at MXN 20. The rollout begins with a 10,000-user pilot and will scale across its 3M users, offering personalized portfolios, zero commissions and 24/7 trading as part of its strategy to democratize investing. 🇲🇽

Deals:

• Mastercard agreed to acquire BVNK for $1.8B, including up to $300M in performance-based payments, as it accelerates expansion into blockchain-based payments. Founded in 2021, BVNK operates in more than 130 countries and provides infrastructure connecting traditional financial systems to blockchain networks, with the deal valuing the company at more than double its previous $750M valuation. 🇺🇸

• Vela LatAm acquired Alfasig, Alpino Tecnologia and ERP Praeter, expanding its ERP and fiscal software vertical with solutions focused on electronic invoicing and tax compliance. The transaction strengthens product integration across fiscal infrastructure and enterprise management systems, bringing Vela LatAm to 26 acquisitions in the region, including 23 in Brazil, as it continues its aggressive M&A strategy. 🇧🇷

General news:

• Cibra is accelerating its open innovation strategy by establishing a dedicated space at Cubo Itaú and launching its Seiva program to collaborate with startups across strategic areas of its operations. The initiative includes partnerships, investments and potential M&A, expanding access to ready-to-market solutions as the company deepens its shift toward external innovation. 🇧🇷

• Tensions between Microsoft and OpenAI are escalating as Microsoft considers legal action over OpenAI’s reported $50B agreements with Amazon, including selecting AWS as the exclusive cloud provider for its new enterprise AI platform, Frontier. The move raises concerns about conflicts with Microsoft’s Azure exclusivity agreement and signals a shift from strategic partnership to direct competition in AI infrastructure and enterprise services. 🇺🇸

• Plata launched as a fully licensed digital bank in Mexico after securing approval from the CNBV, expanding beyond its initial credit card offering to include savings, investment accounts and debit products. The platform has reached 3M users since 2022 and integrates AI-driven infrastructure with a mobile-first experience, positioning itself to accelerate financial inclusion through features such as zero fees, cashback and high credit limits. 🇲🇽

• Accountfy founders launched Mogno, a US-based AI spin-off focused on no-code enterprise app creation, backed by part of the $18M previously raised by the parent company. The startup targets $2M in revenue within its first year and plans an independent $8M seed round in the US, positioning itself beyond finance into broader back-office functions such as HR, legal and operations. 🇺🇸

• Lemon is expanding in Colombia with its Visa Lemon Card, launching a waitlist to drive user growth through a no-fee digital wallet and early-access incentives. The card enables payments in local currency or digital dollars and introduces a 0.4% cashback model linked to the country’s 4×1000 tax, effectively turning a traditional cost into a user benefit. 🇨🇴

• Alive Ventures raised $55M for its second impact fund focused on Colombia and Peru, backed by development finance institutions across Europe and Latin America. The fund has already invested in 11 startups, with 40% allocated to fintechs and additional capital deployed in climate solutions such as solar infrastructure and distributed energy. 🇨🇴

Deals:

• Tess AI raised $5M in a seed round and is relocating to Silicon Valley to accelerate global expansion, targeting $10M in revenue by 2026. The Brazilian-founded platform operates in 25 countries, serving over 16,000 users and enabling no-code agent creation with a task-based pricing model that delivers up to 90% cost savings versus enterprise AI tools. 🇧🇷

General news:

• Early-stage fundraising in Brazil is recovering as startups adapt to stricter governance standards, although raising Series B and beyond remains challenging, pushing companies to seek international capital. Global investors are prioritizing AI-driven startups, while other sectors face lower visibility unless they embed AI to improve productivity and scalability. Despite a more selective environment, top rounds are quickly oversubscribed and valuations are rising, with Mexico gaining share in regional VC flows. 🇧🇷

• Jota is expanding into payments with its voice-enabled solution Fala Tap, allowing users to generate charges via credit, debit and Pix through conversational commands. The fintech reached 150,000 customers and R$2.2B in TPV in its first year and is targeting R$10B in TPV and 1M users by 2026, positioning AI-driven payments as a key differentiator. 🇧🇷

• Blips spun off its financing arm into Finza to scale its embedded credit model beyond proprietary equipment sales after originating more than R$750M in credit. The new platform provides financing infrastructure for industrial partners and targets a R$40M portfolio by the end of 2026, expanding access to productive credit for small businesses. 🇧🇷

• Brazil’s Central Bank is proposing new rules for Open Finance partnerships to address risks related to data sharing beyond regulated environments. The framework introduces stricter requirements on transparency, security and accountability, aiming to standardize data usage and strengthen consumer protection as Open Finance expands. 🇧🇷

• Web Summit will host its first African event in Cape Verde in December 2026, positioning the country as a strategic hub connecting Africa, Europe and the Americas. The initiative aims to integrate local startups and policymakers with global investors, boosting visibility and accelerating the development of the regional tech ecosystem. 🌍

• Santander is expanding Getnet into Colombia to strengthen its presence in Latin America and connect merchants to a unified payments infrastructure. In 2025, Getnet processed more than €238B across 10.5B transactions for 1.2M clients, reinforcing its scale as one of the largest acquirers globally. 🇨🇴

• Bemobi reported strong financial results in Q4 2025 with net revenue reaching R$199.2M (+20.5%) and annual revenue of R$729M (+20%). Growth was driven by a 50% expansion in its payments vertical, with total payment volume rising 36% to R$3.1B and payments and SaaS representing 64.7% of total revenue. 🇧🇷

• OpenAI is developing a desktop super app integrating ChatGPT, Atlas and Codex to unify its ecosystem and accelerate enterprise adoption. The platform will embed autonomous AI capabilities and reduce product fragmentation, reinforcing OpenAI’s strategy to compete in enterprise AI workflows. 🇺🇸

• Jeff Bezos is discussing raising a $100B fund focused on industrial AI to acquire industrial companies and accelerate manufacturing automation. The initiative is linked to Project Prometheus, an AI startup focused on simulating physical environments, and reflects a broader capital shift toward robotics and industrial AI. 🇺🇸

Deals:

• Kalshi is raising $1B in a new funding round led by Coatue, doubling its valuation to $22B from $11B in December as prediction markets gain traction amid rising trading volumes. Growth has been driven by sports, geopolitics and market-based contracts, with sports accounting for about half of total volume, signaling increasing mainstream adoption despite ongoing regulatory scrutiny. The sector continues to face legal challenges at the state level, while competitors like Polymarket expand through partnerships such as Major League Baseball. 🇺🇸

• Rexi raised $1.2M in a pre-seed round to scale its AI-native financial reconciliation platform. The solution automates workflows with 99.7% accuracy and reduces processing time from days to minutes, targeting banks, fintechs and payment processors across Latin America and North America. 🇺🇸

• Core AI raised $4.1M to scale its credit modeling platform, integrating with banking-as-a-service providers to improve approval rates while maintaining low default levels. The company uses behavioral and transactional data to automate underwriting and credit operations, targeting expansion across financial services. 🇧🇷

• OpenAI is acquiring Python tooling company Astral to strengthen its developer ecosystem and enhance Codex, which has surpassed 2M weekly active users. The acquisition supports OpenAI’s strategy to expand into enterprise-grade development workflows and compete more directly with Anthropic. 🇺🇸

General news:

• Pismo is deepening its integration within Visa as it transitions from an independent fintech into a core technology layer of the company’s global banking infrastructure, combining organizational restructuring with continued hiring in engineering, cybersecurity and product. The platform is already enabling new financial products, including a corporate card launched in Chile with BICE and Mendel that integrates financing, expense management and Visa’s network into a single cloud-native solution with real-time controls and customization capabilities. The move highlights Visa’s strategy to scale embedded financial infrastructure globally while maintaining a strong focus on product innovation and enterprise use cases. 🌎

• Brazil’s Central Bank reported a new Pix data security incident involving 28,203 keys linked to Pefisa, bringing total exposed keys in 2026 to over 33,500. The breach affected only registration data and did not compromise balances or transactions, but reinforces ongoing regulatory scrutiny as instant payments scale. 🇧🇷

• Brazil’s acquiring market remains dominated by incumbents, with Rede gaining 5 percentage points in users to reach 25% share and leading transaction volume at 18%. Cielo maintained leadership at 28%, while PagBank reached 26%, as Mercado Pago strengthened cross-sell performance and newer entrants struggled to gain share. 🇧🇷

• Crypto.com is laying off 12% of its workforce as it integrates AI to improve efficiency amid a weaker crypto market. The move aligns with broader industry trends, as companies optimize operations and reposition around AI-driven productivity while crypto prices remain below recent peaks. 🌍

• Nuvocargo launched an AI-native freight execution platform targeting logistics across the US, Mexico and Canada. The solution reduces freight costs by 7%–20% through automation and pricing optimization, while integrating with a network of over 300,000 carriers and managing more than 100,000 shipments. 🇺🇸

• AI is reshaping early-stage startups through “founder mode”, reducing the time from MVP to R$100K in monthly revenue by up to 20%. Lean teams of three to six people are now achieving output comparable to larger organizations, with AI accelerating execution across product, marketing and sales while increasing competition. 🇧🇷

• PicPay shares fell sharply despite strong results, dropping up to 15% after a previous 22% decline amid post-IPO rotation and macro-driven risk aversion. The company reported R$188M in net income in Q4 2025 (+182% YoY) and strong credit growth, but rising default rates and strategic shifts added uncertainty for investors. 🇧🇷

• Microsoft developed GigaTIME to improve cancer immunotherapy, an AI platform that maps tumor microenvironments using standard pathology images. Trained on 40 million cells and validated across 14,000+ patients, the system can reduce diagnostic costs and improve treatment targeting, advancing precision oncology at scale. 🇺🇸

Deals:

• Ume raised R$150M through a feeder FIDC backed by investors including Itaú BBA, Bradesco BBI and Credit Saison to expand its retail credit operations. The structure enables customized credit vehicles for partner retailers, improving margins and risk management while supporting scalable credit infrastructure growth. 🇧🇷

• Zolvo raised $500K from Y Combinator to scale its AI-native platform for invoice reconciliation and commercial credit operations. The solution automates verification and reporting, delivering over 60% cost reduction while already managing more than $1B in assets, positioning the company as infrastructure for commercial lending. 🇨🇴

NVIDIA GTC reinforces AI as infrastructure

NVIDIA’s annual GTC conference once again positioned the company at the center of the global AI ecosystem — and, more importantly, reinforced a key shift: AI is no longer just about models, it is now about infrastructure at scale.

The headline announcement was the Vera Rubin platform, NVIDIA’s next-generation AI architecture, which goes beyond GPUs to offer a fully integrated system (CPU + GPU + networking + software) designed specifically for the era of agentic AI and large-scale inference. This reflects a broader transition in the industry from training models to running them continuously in production.

A major theme throughout the keynote was inference as the next battleground. As AI moves from experimentation to real-world deployment, the demand is shifting toward systems that can serve millions of users in real time. NVIDIA explicitly framed this as a $1 trillion opportunity in AI infrastructure by 2027, significantly increasing prior expectations.

Closely tied to this was the concept of “AI factories” — large-scale, industrialized data centers designed to run continuous AI workloads, rather than traditional cloud infrastructure. These systems are being built at unprecedented scale, with rack-level architectures and tightly integrated components, reinforcing the idea that AI compute is becoming a core layer of the global economy.

Another key shift highlighted at GTC was the move from chatbots to autonomous agents. NVIDIA introduced new frameworks (such as NemoClaw) aimed at enabling AI systems that can take actions, not just generate responses, signaling the next phase of AI adoption across enterprises.

Finally, the company continued to expand beyond chips into a full-stack AI platform, spanning hardware, software, networking, and developer tools. The message was clear: the winners in AI will be those who control the entire stack — not just the models.

Key takeaway

GTC 2026 confirmed that the AI race is shifting from building models to scaling infrastructure — with inference, autonomous agents, and vertically integrated systems emerging as the next phase of the cycle.

South Summit Brazil 2026

Date: March 25–27, 2026

Location: Porto Alegre, Brazil

Description: A global innovation platform connecting startups, corporations, and investors to foster entrepreneurship and scalable business growth.

More infoBrazil at Silicon Valley 2026

Date: April 6–8, 2026

Location: Sunnyvale, CA, USA

Description: A conference connecting Brazilian leaders and entrepreneurs with Silicon Valley to promote innovation, investment, and cross-border business.

More infoVTEX Day 2026

Date: April 16–17, 2026

Location: São Paulo, Brazil

Description: One of the world’s largest digital commerce events, bringing together global retail leaders, brands, and technology innovators.

More infoGramado Summit 2026

Date: May 6–8, 2026

Location: Gramado, Brazil

Description: A technology and innovation festival combining business, strategy, marketing, and public-sector innovation discussions.

More infoRIO2C 2026

Date: May 26–June 1, 2026

Location: Rio de Janeiro, Brazil

Description: A creativity-driven event connecting technology, media, audiovisual, music, sustainability, and entrepreneurship.

More infoSouth Summit Madrid 2026

Date: June 3–5, 2026

Location: Madrid, Spain

Description: A global innovation conference connecting startups seeking scale with investors and corporations looking for new opportunities.

More infoWeb Summit Rio 2026

Date: June 8–11, 2026

Location: Rio de Janeiro, Brazil

Description: Part of the Web Summit global series, the event connects startups, investors, and tech leaders across Latin America.

More infoFebraban Tech 2026

Date: June 24–26, 2026

Location: São Paulo, Brazil

Description: One of the main financial technology and innovation events for the banking and financial services sector in Latin America.

More info

See links on the intro - Carta & Pitchbook

“AI is no longer a single breakthrough or application — it is essential infrastructure.” — Jensen Huang